Dynamic Programming for Estimating Acceptance Probability of Credit Card Products ()

1. Introduction

Traditionally, credit card issuers charged a “fixed interest rate” on their credit cards for all their customers. According to [1] , since 1991 however, some credit card firms have switched to “variable interest rate” as a result to the credit card lending market becoming more competitive [1] . As reported by [2] , profitability of credit card lenders consequently suffered a substantial loss due to this competition.

Hence it is becoming increasing important to be able to secure the acceptance of an offer in order to have profit. So, the lenders have to be able to “persuade” the customer to accept their offer. When a good customer is willing to accept an offer, he or she will generate profit to an organisation. One way of doing so is to “customise” the offer to the customer. The lenders could use information about the customer’s preferences so as a guide to make a decision on what type of offer the customer may be interested in. This information is already available from initial collection for credit scoring purposes. By looking at which type of product accepted by different customers, the lenders can “learn” about the preferences of their customers. Hence, the decision on what offer to make can be modeled.

There are a number of researchers who have researched acceptance probability for financial products to maximise profitability; for example [3] [4] [5] .

In this paper, the authors extended an acceptance model based on the work done by [4] . The lender’s decision problem has been modeled as a Markov Decision Process under uncertainty. The objective of this model is the maximisation of profit using a dynamic programming [6] model with Bayesian updating to incorporate the usage of past customer information to optimise acceptance probability. The problem is discussed in the next section. Then the optimal solutions for variants of products are described. Finally, the numerical results are tabled and the conclusions are drawn in the last section.

2. The Problem

Banks have many variants of a personal financial product which they can offer to their customers. The attractiveness of the variants to the customer can be ordered in such a way that the likelihood of accepting that variant by the customer is monotonically decreasing while the lender’s profitability of the variant is monotonically increasing. For example, a credit card with different interest rates likes 5%, 10% and so on. The decision on which offer to make to the next applicant is based on the given knowledge of the previous offers and whether the offer accepted by previous customers. The objective of modeling the acceptance probability is to maximise the profit to the bank.

In the model here, the authors follow the example of [4] and model the problem as a credit card product with different variant of interest rates. It is assumed that the customers are from homogenous population and the probability of any customer choosing variant t is

where

and

. The profit to the lender of t variant chosen by customers is

where

and

. Thus, the bank’s maximum profit is determined by

. However, one does not know the probability of

, so we defined

as with the condition of

. Here assume Offer 1 is a credit card with 5% interest rate annually, Offer 2 is a credit card with 10% interest rate annually, Offer 3 is a credit card with 15% interest rate annually and Offer 4 is a credit card with 20% interest rate annually. Also, assume the number of potential customers has a geometric distribution with parameter β with the last customer is 1 − β.

At the beginning, two variants of the credit cards are considered in the model. There are a few assumptions made in this model. First, assume that if a customer rejected variant t, meaning that he/she would also reject all worse variants u, where

. Similarly, if a customer accepted variant t, he/she would accepted all better variants v, where

. With so

. To illustrate, let u = 20% interest rate on a credit card, t = 10% and v = 5%. If one rejects an offer of 10% interest rate (t), then one is also likely to reject a credit card of 15% interest rate (u). And if one accepts the offer of 10% interest rate, one is likely to accept a “better offer” of 5% (v) interest rate. We ensure this by defining a set of conditional probabilities where

is the probability of accepting Offer 1 and

is the Bernoulli random variable.

;

= Probability (customer would accept Offer 2/customer would accept Offer 1).

Since

,

hence

.

This condition ensures that

.

For three variants of interest rates for the credit card, the conditional probability is as follows:

Since

,

hence

and this ensures that

.

And so for the four variants of interest rates for the credit card, the conditional probability is as follows:

Since

,

hence

and this ensures that

.

For many variants of interest rates for the credit card, the conditional probability is defined as:

,

where

= Probability of accepting offer m,

= Probability (customer would accept Offer m/customer would accept Offer

).

This condition ensures that

.

Given that

are all Bernoulli random variables so in a Bayesian setting, one could describe the bank’s knowledge of the information as a Beta distribution. The prior for

is by

whose probability density function is

and expectation is

where

= the number of customers

that have accepted the offer t and

= the number of customers who were extended offer t. At any point, the bank’s belief about the acceptance probabilities

is given by the parameters

. Let the expected maximum total future profit to the bank as

given that the current belief is

.

are the parameters of the Beta distribution describing one’s belief of

. So if Offer 1 is accepted, the parameters will get updated to

,

. If it is rejected, they get updated to

,

. Thus, one could reinterpret these as:

= number of customer who already accepted Offer 1 (Offer 5% in this model); and

= number of customer who have been offered Offer 1 (Offer 5%).

Hence

are the parameters of the Beta distribution describing one’s belief of

. Note the assumption that the offer of Offer 1 will have to be accepted first before Offer 2 can be considered. If Offer 2 is accepted, the parameters get updated to

,

. So when it is rejected, they get updated to

,

. Thus,

= number of customer who already accepted Offer 2 (Offer 10% in this model); and

= number of customer who have been offered Offer 2 (Offer 10%).

Note that

are the parameters of the Beta distribution describing one’s belief of

. If Offer 3 is accepted, the parameters get updated to

,

. When Offer 3 is rejected, and the customer is assumed to would have accepted Offer 1 but could reject Offer 2; or accepted Offer 1 and Offer 2. Hence they get updated to

,

and the

and

is updated depending on the conditions of Offer 1 and Offer 2. Thus,

= number of customer who already accepted Offer 3 (Offer 15% in this model); and

= number of customer who have been offered Offer 3 (Offer 15%).

are the parameters of the Beta distribution describing one’s belief of

. If Offer 4 is accepted, the parameters get updated to

,

. If it is rejected, then there are three possibilities:

1) The customer would have accepted Offer 1 but rejected Offer 2 and Offer 3;

2) The customer would have accepted Offer 1 and Offer 2 but rejected Offer 3;

3) The customer would have accepted Offer 1, Offer 2 and Offer 3. Thus,

= number of customer who already accepted Offer 4 (Offer 20% in this model); and

= number of customer who have been offered Offer 4 (Offer 20%).

In the above four cases,

for

.

By including the information obtained from the past acceptance and rejection of each variants of the product, the model becomes a “learning” model to support making decisions on which product to offer to the next customer.

With such a belief distribution, the expected probability of Offer 1 being

accepted is

, Offer 2 is

, Offer 3 is

and Offer 4 is

. For k offers, this is defined as

.

Let

= expected maximum future profit from the next customer. Consider a two variant case, given that one has to choose which of the two variants of the product to offer to the next customer, function

has to satisfy the optimal equation (see [7] ):

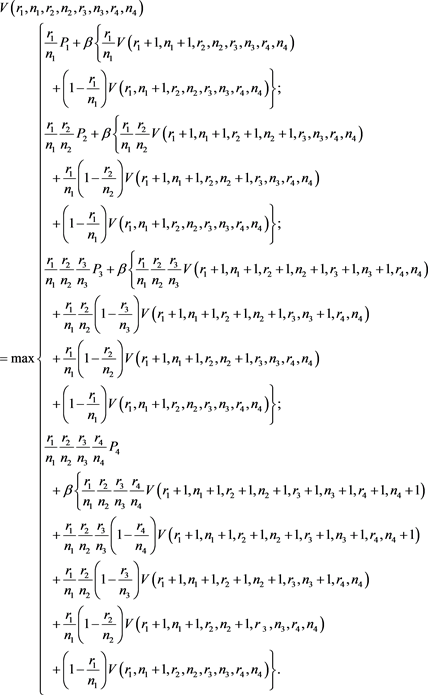

(1)

For the 3 variants of the credit card product, function

satisfies the optimal equation of:

(2)

For the 4 variants of the credit card product, function

satisfies the optimal equation of:

(3)

(3)

For m variants of products, function

satisfies the optimal equation:

(4)

The first term in each offer is the probability that a customer will accept the variant offered multiplied by the profit to the bank. The remaining terms depends on the chance β that there will be another customer. In the β equation, the first term corresponds to the current offer being accepted. The remaining terms correspond to the offer being refused and it looks at the different ways it can happen. For example, the term

corresponds to the refusal of the Offer 2. While

means one believes Offer 1 has been refused thus there is no updating of Offer 2. The term

corresponds to the refusal of the l-th offer.

3. Optimal Solution for Many Variants of the Product

Consider a variation of the problem in (1) where the lender has a cost of

if an offer is made to a customer where the state is

irrespectively of which offer is made. Since the cost is independent of the offer made, it cannot affect the optimal action. Let

be the optimal expected profit for the modified problem. Then, we know the optimal policy when solving for

is the same as for

, with

(5)

where

,

, and

.

For the 3 variants case, the optimal expected profit is defined as:

(6)

where

,

.

For the 4 variants case, the optimal expected profit is defined as:

(7)

where

,

.

Recall that Equation (4) is the optimal equation for m variants of the product which is the extension of Equations (1)-(3) in the 2, 3 and 4-variants cases

respectively. We subtract a cost of

from all

the actions in state of

of Equations (5)-(7). We know that this cannot affect the decisions made but allows us to simplify Equations (5), (6) and (7) to a general equation of:

(8)

The proof of the theorem can be referred in Seow and Thomas [6] .

If we have 2 variants,

1)

, one chooses Offer 1.

2)

, one chooses Offer 2.

If we have 3 variants,

1)

, one chooses Offer 1.

2)

, one chooses Offer 2.

3)

, one chooses Offer 3.

If we have 4 variants,

1)

, one chooses Offer 1.

2)

, one chooses Offer 2.

3)

, one chooses Offer 3.

4)

, one chooses Offer 4.

So, if we have m variants, from the theorem as in [4] it is found that:

At any state

, there exists functions

so that:

1) One chooses Offer 1 to all future customers if

;

2) One chooses Offer 2 to all future customers if

;

3) One chooses Offer t to all future customers if

; and

4) One chooses Offer t + 1 to all future customers if

.

We have proved that there is exists at most one

in the following Lemma 1.

Lemma 1:

At any state

, there is exists at most one

for the choice of t variants of all future customers.

Proof

To prove the Lemma above, we need to consider two cases.

Case 1 where there is exactly one switch:

1) Let P(m) be the statement that one chooses Offer t to all future customers if

and one chooses Offer

to all future customers if

.

2) Let P(1) which is base offer be the default. Hence for m = 1, one chooses Offer 1.

3) For m = 2, assume P(2) is correct, that is:

a)

, one chooses Offer 1.

b)

, one chooses Offer 2.

Note that there is one

.

For the following statements,

is used to differentiate

since

are not the point to switch the offer.

4) Suppose P(K) is true, for m = K, where P(K) is the statement that one chooses Offer t to all future customers if

; and one chooses Offer t + 1 to all future customers if

. P(K) also means that:

a) One chooses Offer 1 if

.

b) One chooses Offer 1 if

and one chooses Offer 2 if

.

c) One chooses Offer 1 if

; one chooses Offer 2 if

; and one chooses Offer 3 if

.

d) One chooses Offer 1 if

; one chooses Offer 2 if

; one chooses Offer 3 if

; one chooses Offer 4 if

; and so on, then one chooses Offer t if

.

e) One chooses Offer

if

and there is one

or switch of offers.

5) It can be shown that

is true where

is the statement that one chooses Offer t to all future customers if

, otherwise one chooses Offer

to all future customers if

.

also means that:

a) One chooses Offer 1 if

.

b) One chooses Offer 1 if

and one chooses Offer 2 if

.

c) One chooses Offer 1 if

; one chooses Offer 2 if

; and one chooses Offer 3 if

.

d) One chooses Offer 1 if

; one chooses Offer 2 if

; one chooses Offer 3 if

; one chooses Offer 4 if

; and so on, then one chooses Offer t if

.

e) One chooses Offer

if

.

Since P(K) is true, that is:

1) One chooses Offer 1 if

.

2) One chooses Offer 1 if

and one chooses Offer 2 if

.

3) One chooses Offer 1 if

; one chooses Offer 2 if

; and one chooses Offer 3 if

.

4) One chooses Offer 1 if

; one chooses Offer 2 if

; one chooses Offer 3 if

; one chooses Offer 4 if

; and so on, then one chooses Offer t if

The introduction of an additional option of choice; the term

in (5, d); can also be expressed as

. Since

has an additional option choice of

, then the next choice is one chooses variant t to all future customers if

before it comes to the last condition of choice which is where one chooses variant t + 1 if

. Hence, P(K + 1) is also true, that is:

1) One chooses Offer 1 if

.

2) One chooses Offer 1 if

and one chooses Offer 2 if

.

3) One chooses Offer 1 if

; one chooses Offer 2 if

; and one chooses Offer 3 if

.

4) One chooses Offer 1 if

; one chooses Offer 2 if

; one chooses Offer 3 if

; one chooses Offer 4 if

; and so on, then one chooses Offer t if

.

5) One chooses Offer

if

and there is one

.

Case 2 where there is no change in the decision of offer.

If there is no change in the decision of the offer, from above proof of case 1 means that there is only one variant at any state and

does not exist trivially.

4. Empirical Results and Analysis

In this section, the data needed to get information for learning the switch of offers has been generated using the dynamic programming model. This is based on expected profit generated (in ₤). Some results generated by the model are shown in the following tables. We first defined β = 0.5 for 2 and 3 variants in the model. Then defined β = 0.999 for 4 variants. We have subtracted the “fee” from the model, hence the values shown are not the full profits. Please note the choice of β = 0.5 and 0.999 was based on the purpose to illustrate the profit generated at 50% discounting factor and almost 100% discounting factor.

4.1. Two Variants Case

If there are 2 variant of products (5% and 10% interest rates), then variant 5%

will be chosen if

and otherwise, variant 10% will be chosen if

.

Table 1 and Table 2 present some of the results generated by the model. The bold in the row is the point when the switch of offers occurs. We choose

and

to represent a case where one’s belief of the acceptance of variant

5% is

.

![]()

Table 1. Part of results generated by the acceptance model when P1 = 10.000, P2 = 25.000, β = 0.5, m = 45, p = 10.

![]()

Table 2. Part of results generated by the acceptance model when P1 = 10.000, P2 = 25.000, β = 0.5, m = 45, p = 10.

Table 3 and Table 4 present a case where one’s belief of the acceptance of

variant 5% with the ratio of

and some of the belief points at which the

offer decision changes.

Table 5 and Table 6 present a case where one’s belief of the acceptance of

variant 5% with the ratio of

and some of the belief points at which the

offer decision changes.

Table 7 and Table 8 show an example where there is no any point of the switch of offers occurs. That is

does not exists in any state. We choose

and

to represent a case where one’s belief of the

acceptance of variant 10% is

.

![]()

Table 3. Changing of offers when r1 = 1, n1 = 2, P1 = 10.000, P2 = 25.000, β = 0.5, m = 45, p = 10.

![]()

Table 4. Changing of offers when r1 = 8, n1 = 16, P1 = 10.000, P2 = 25.000, β = 0.5, m = 45, p = 10.

![]()

Table 5. Changing of offers when r1 = 5, n1 = 6, P1 = 10.000, P2 = 25.000, β = 0.5, m = 45, p = 10.

![]()

Table 6. Changing of offers when r1 = 15, n1 = 18, P1 = 10.000, P2 = 25.000, β = 0.5, m = 45, p = 10.

![]()

Table 7. Offer 5% to all future customers when P1 = 20.000, P2 = 50.000, β = 0.999, m = 45, p = 10.

![]()

Table 8. Offer 10% to all future customers when P1 = 20.000, P2 = 50.000, β = 0.999, m = 45, p = 10.

4.2. Three Variants Case

If there are 3 variant of products (5%, 10% and 15% interest rates), then variant

5% will be chosen if

and

. Variant 10% will be chosen if

and

. Otherwise, variant 15% will be chosen if

and

.

Table 9 and Table 10 presented some of the results generated by the model for three variant of products. The bold in the row is the point when the switch of offers occurs. We choose

and

to represent a case where one’s

belief of the acceptance of variant 5% and variant 10% are

. The

changes of offer shown are from variant 5% to variant 15%.

Table 11 presents some of the results generated by the model for three variants of the product. The bold row is the point when the switch of offers occurs. We choose

and

to represent a case where one’s belief

of the acceptance of variant 5% and 15% are

and

respectively.

The changes of offer are from variant 5% to variant 10%.

![]()

Table 9. Part of results generated by the acceptance model when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 10. Part of results generated by the acceptance model when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 11. Part of results generated by the acceptance model when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

Table 12 presents some of the results generated by the model for three variants of the product. The bold row is the point when the switch of offers occurs. We choose

and

to represent a case where one’s

belief of the acceptance of variant 5% and 10% are

and

respectively.

Table 13 and Table 14 present a case where one’s belief of the acceptance of

variant 5% with the ratio of

and acceptance of variant 10% with

the ratio of

respectively for some of the belief points at which the

offer decision changes.

Tables 15-17, presented here show that there is no any point of the switch of offers occurs. That is

does not exists in any state of

. In Table 15, we choose

and

to represent a case

where one’s belief of the acceptance of variant 10% is

and acceptance

of variant 15% is

. In Table 16, we choose

and

to represent a case where one’s belief of the acceptance of variant

10% is

and acceptance of variant 15% is

. In Table 17, we

choose

and

to represent a case where one’s belief

![]()

Table 12. Part of results generated by the acceptance model when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 13. Changing of offers when r5 = 4, n5 = 5, r10 = 4, n10 = 5, P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 14. Changing of offers when r5 = 6, n5 = 16, r10 = 6, n10 = 16, P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 15. Offer 5% to all future customers when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 16. Offer 10% to all future customers when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

![]()

Table 17. Offer 15% to all future customers when P1 = 10.000, P2 = 25.000, P3 = 35.000, β = 0.5, m = 6, p = 6.

of the acceptance of variant 10% is

and acceptance of variant 15% is

.

Table 18 shows that as r1 increases but the rate

and

are fixed, the

crucial value where one changes offers,

, is monotonically non increasing. We also give results for the effect of more information (increment of

![]()

Table 18. Effect of more information on the switch of offers.

r2) in the table. The

for n2 varying from 1 to 16. Note that the hyphen (−) in the table means that there is no changes of the offer occurs where Offer 5% is the only offer.

4.3. Four Variants Case

If there are 4 variants of products, then variant 5% will be chosen if

,

, and

. Variant 10% will be chosen if

,

, and

. Variant 15% will be chosen if

,

, and

. Otherwise, variant 20% will be chosen if

,

, and

.

Table 19 presents some of the results generated by the model for four variants of the product. The bold row is the point when the switch of offers occurs. We choose

,

, and

to represent a case where one’s belief of the acceptance of variant 5%, 15% and 20% are

and

respectively. The changes of offer are from variant 5% to variant 10%.

Table 20 presents some of the results generated by the model for four variants of the products. The bold row is the point when the switch of offers occurs. We choose

,

and

to represent a case where

one’s belief of the acceptance of variant 5%, 10% and 20% are

and

respectively. The changes of offer shown is from variant 5% to variant

15%.

Table 21 presents some of the results generated by the model for four variants of the products. The bold row is the point when the switch of offers occurs. We

![]()

Table 19. Part of results generated by the acceptance model when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 20. Part of results generated by the acceptance model when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 21. Part of results generated by the acceptance model when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

choose

,

, and

to represent a case where

one’s belief of the acceptance of variant 5%, 10% and 20% are

and

respectively. The changes of offer shown is from variant 5% to

variant 20%.

Tables 22-24 shown that the changes of offer is from variant 10% to variant 15%, variant 10% to variant 20% and variant 15% to variant 20% respectively.

Tables 25-28 presented here show no point for the switch of offers. That is

does not exist in any state of

.

![]()

Table 22. Part of results generated by the acceptance model when. P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 23. Part of results generated by the acceptance model when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 24. Part of results generated by the acceptance model when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 25. Offer 5% to all future customers when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 26. Offer 10% to all future customers when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 27. Offer 15% to all future customers when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

![]()

Table 28. Offer 20% to all future customers when P1 = 20.000, P2 = 50.000, P3 = 80.000, P4 = 100.000, β = 0.999, m = 3, p = 2.

5. Conclusion

From the results, we can clearly see that there is at most one point of switch offers. No matter how many variants of the product offered, the switching offer will not more than one. Based on this observation, the model can tell the best offer to extend to the next customer in an efficient manner and maximise the profit earned. Hence the model is able to identify the best offer for variants of credit cards. Further research would be to test this on different financial products like mortgages.

Acknowledgements

This research is supported by the Research University Grant Scheme (RUGS) 05-02-12-1869RU.

Disclosure Policy

The authors declare that there is no conflict of interest regarding the publication of this paper.