Wavelet Density Estimation and Statistical Evidences Role for a GARCH Model in the Weighted Distribution ()

1. Introduction

We suppose that  is a sample of a strictly stationary and exponentially strongly mixing process

is a sample of a strictly stationary and exponentially strongly mixing process  where, for any

where, for any ,

,

(1)

(1)

is a sequence of identically distributed random variables with common known density

is a sequence of identically distributed random variables with common known density  and

and  is a sequence of identically distributed random variables with common unknown density

is a sequence of identically distributed random variables with common unknown density . For any

. For any ,

,  and

and  are independent. We suppose that

are independent. We suppose that  is a weighted density of the form

is a weighted density of the form

(2)

(2)

where  is a known positive function,

is a known positive function,  an unknown density of a random variable

an unknown density of a random variable  and

and  is the unknown normalization parameter:

is the unknown normalization parameter:

Our goal is to estimate  when only

when only  are observed. The Equation (1) is a GARCH-type time series model classically encountered in financial models see [1] and practical examples of Equation (2) can be found in e.g. [2-4].

are observed. The Equation (1) is a GARCH-type time series model classically encountered in financial models see [1] and practical examples of Equation (2) can be found in e.g. [2-4].

In this article, we construct a linear wavelet estimator and measure its performance by determining upper bounds of the mean integrated squared error (MISE) over Besov space.

In what follows, we have also surveyed the role of data and evidential inference in the model. The data play a very important essential role in statistical analysis, to the extent that many statistical researchers believe in the famous saying: “Ask the data.” We consider the Test

(3)

(3)

for the model and we evaluate the sensitivity of the value in the test hypotheses. In this test, the evaluation criterion is the area between the curves of the cumulative distribution functions under  and

and  hypotheses. Details on evidential inference can be found in [5,6]. Also [7] have studied about Comparing of record data and random observation based on statistical evidence.

hypotheses. Details on evidential inference can be found in [5,6]. Also [7] have studied about Comparing of record data and random observation based on statistical evidence.

Through the rest of the paper, at first assumptions and then an introduction about wavelets are presented in Section 2. The estimators and results are given in Section 3. In Section 4, general explanations regarding evidential inference and its application in a test. The proofs are gathered in Section 5.

2. Assumptions and Wavelets

2.1. Assumptions

We formulate the following assumptions:

• Without loss of generality, we assume that  and

and

have the support

have the support  and

and  where

where

•

• We suppose that for any , the

, the  -th strongly mixing coefficient of

-th strongly mixing coefficient of  by

by

where, for any , let

, let  be the

be the  -algebra generated by

-algebra generated by  and

and  is the

is the  -algebra generated by

-algebra generated by .

.

We suppose that there exist three (known) constants,  and

and  such that

such that

This assumption is satisfied by a large class of GARCH processes. See e.g. [8-10].

• For any , it follows from the independence of

, it follows from the independence of  and

and  that the density of

that the density of  is

is

•

• We suppose that there exists two constants,  and

and , such that

, such that

(4)

(4)

and

(5)

(5)

2.2. Wavelets and Besov Balls

Let  be a positive integer, and

be a positive integer, and  and

and  be the Daubechies wavelets

be the Daubechies wavelets  which satisfy

which satisfy

.

.

Set

Then, there exists an integer  such that, for any integer

such that, for any integer , the collection

, the collection

is an orthonormal basis of  (the space of squareintegrable functions on 0,1). We refer to [11].

(the space of squareintegrable functions on 0,1). We refer to [11].

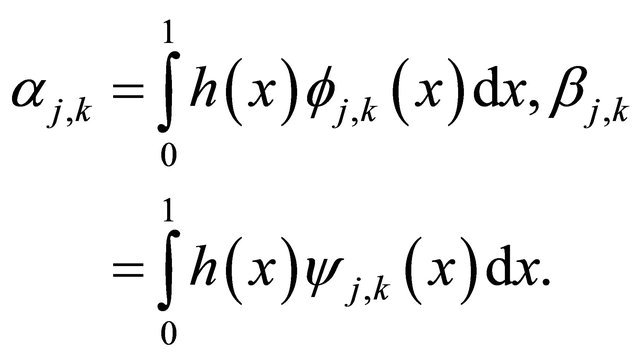

For any integer , any

, any  can be expanded on

can be expanded on  as

as

where  and

and  are the wavelet coefficients of

are the wavelet coefficients of  defined by

defined by

(6)

(6)

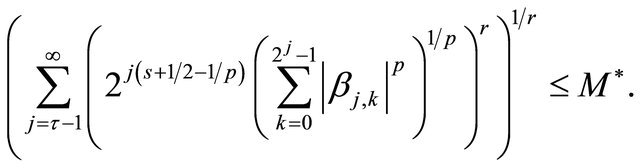

Let  and

and . A function

. A function  belongs to

belongs to  if and only if there exists a constant

if and only if there exists a constant  (depending on

(depending on ) such that the associated wavelet coefficients Equation (6) satisfy

) such that the associated wavelet coefficients Equation (6) satisfy

We set . Details on Besov balls can be found in [12].

. Details on Besov balls can be found in [12].

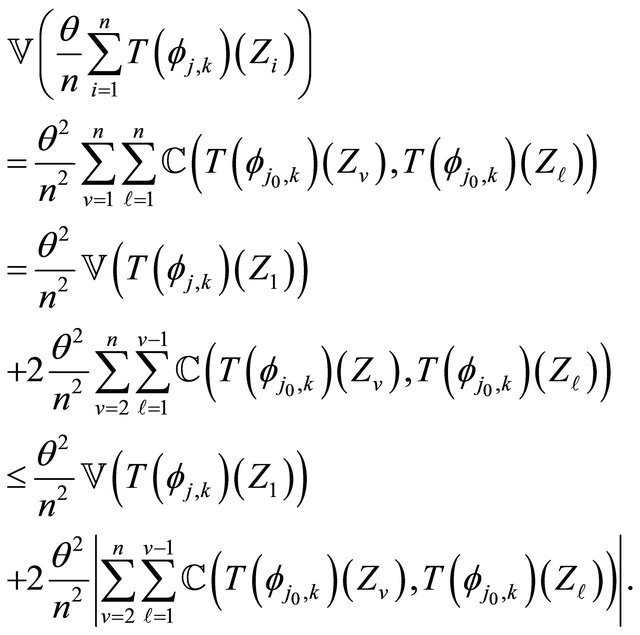

3. Estimators and Results

Firstly, we consider the following estimator for

(7)

(7)

Then, for any integer  and any

and any , we estimate

, we estimate

(8)

(8)

where, for any ,

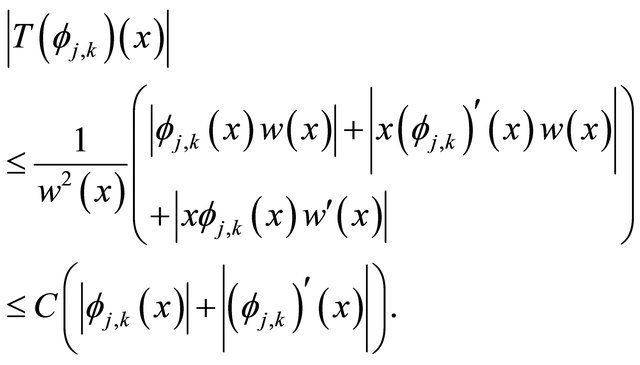

,  is the operator

is the operator

(9)

(9)

and

and  are similar with multiplicative censoring model (see [13]).

are similar with multiplicative censoring model (see [13]).

We are now in the position to define the considered estimators for . Suppose that

. Suppose that . We define the linear estimator

. We define the linear estimator  by

by

(10)

(10)

where  is defined by Equation (8) and

is defined by Equation (8) and  is the integer satisfying

is the integer satisfying

(11)

(11)

• Lemma 3.1

• Let  be Equation (7) and

be Equation (7) and . Then we have

. Then we have

•

• Let  be Equation (1),

be Equation (1),  be Equation (9) and for any integer

be Equation (9) and for any integer  and any

and any ,

,

. Then we have

. Then we have

•

• For any integer  and any

and any , let

, let

be Equation (8) and

be Equation (8) and .

.

Then, under the assumptions of Subsection 2.1, there exists a constant  such that

such that

Proposition 3.1 For any integer  and any

and any  Then, under the assumptions of Subsection 2.1•

Then, under the assumptions of Subsection 2.1•

Proposition 3.2 Let , for any integer

, for any integer  and any

and any , let

, let  be Equation (8) and

be Equation (8) and

. Then• there exists a constant

. Then• there exists a constant  such that

such that

•

• there exists a constant  such that

such that

•

• there exists a constant  such that

such that

Theorem 3.1 (Upper bound for ) Consider Equation (1) under the assumptions of Subsection 2.1. Suppose that

) Consider Equation (1) under the assumptions of Subsection 2.1. Suppose that  with

with . For any

. For any

and

and  be Equation (10), then there exists a constant

be Equation (10), then there exists a constant  such that

such that

Remark that  is the slower than the optimal one in the standard density estimation problem i.e.

is the slower than the optimal one in the standard density estimation problem i.e.  (see e.g. [14, Chapter 10]). This deterioration is due to the presence of GARCH model and weighted distribution.

(see e.g. [14, Chapter 10]). This deterioration is due to the presence of GARCH model and weighted distribution.

4. Statistical Evidence

4.1. Statistical Inference

The evidential approach to statistical inference concerns a novel approach in statistical analysis. Evidential inference is solely based on data as evidence and calculation of the evidence strength. It is not influenced by mental and personal components and factors such as former beliefs and loss functions. Using evidential inference in the model Equation (1), we will survey when censoring of data will lead to considerable data loss, and we will determine the time when data is lost by determining an appropriate criterion. In the model for

for , the data observed from the variable

, the data observed from the variable  are denoted by the subscript (cen), and the data observed from the variable

are denoted by the subscript (cen), and the data observed from the variable  are denoted by the subscript (ncen). Considering the Test Equation (3) in the above model, due to the symmetry of the test hypotheses in evidential methods and without losing the generality of the problem, the value of is assumed to be

are denoted by the subscript (ncen). Considering the Test Equation (3) in the above model, due to the symmetry of the test hypotheses in evidential methods and without losing the generality of the problem, the value of is assumed to be . In order to support

. In order to support  and

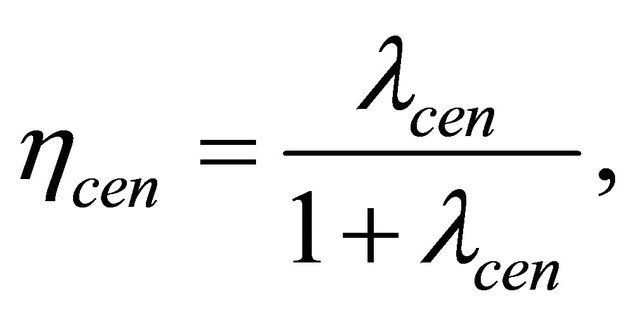

and  hypotheses, we now use the following criterion:

hypotheses, we now use the following criterion:

(12)

(12)

where  and

and  are the measure of expected true evidence in the censored and uncensored data respectively, and

are the measure of expected true evidence in the censored and uncensored data respectively, and  is the criterion of the support of data from

is the criterion of the support of data from  hypothesis against

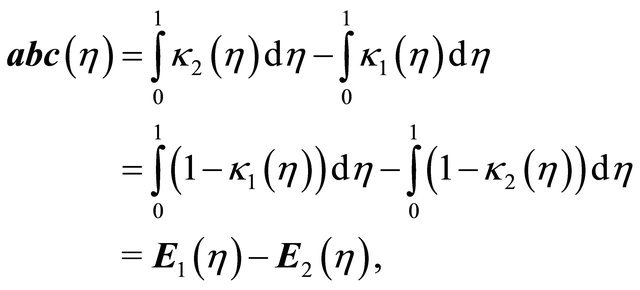

hypothesis against  hypothesis. This support criterion is optimal when the area between the two curves of

hypothesis. This support criterion is optimal when the area between the two curves of  cumulative functions under

cumulative functions under  and

and  is maximum, please see [15]. This area which is denoted by

is maximum, please see [15]. This area which is denoted by  in the form of

in the form of

where  is the cumulative distribution function of

is the cumulative distribution function of  and

and  is the mean value of

is the mean value of  under

under  hypotheses. In view of [6], the support criterion

hypotheses. In view of [6], the support criterion  is defined as follows:

is defined as follows:

(13)

(13)

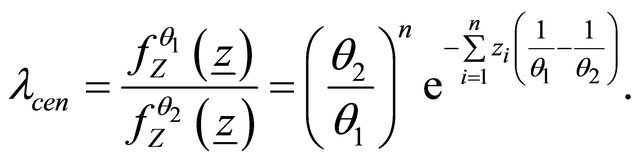

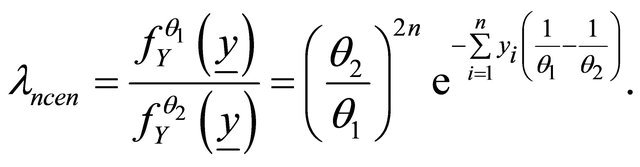

where  is the likelihood ratio and for the two censored and uncensored cases we have

is the likelihood ratio and for the two censored and uncensored cases we have

(14)

(14)

where  and

and  are likelihood functions for

are likelihood functions for  and

and  variables respectively, in the Equation (1) under

variables respectively, in the Equation (1) under  hypotheses.

hypotheses.

4.2. Measuring Statistical Evidence

We consider i.i.d case for variables in the Equations (1) and (2), also set  and then, we investigate the behavior of

and then, we investigate the behavior of  by means of simulation. In addition, we analyze

by means of simulation. In addition, we analyze  and

and  hypotheses in Test Equation (3) by determining support criterion

hypotheses in Test Equation (3) by determining support criterion  of the measure of expected true evidence

of the measure of expected true evidence . The programming codes of this part are written in the MAPLE (15) environment.

. The programming codes of this part are written in the MAPLE (15) environment.

Example 1. In this example, we generate data from gamma and uniform distribution as follows, considering multiplicative censoring model:

Then, according to Equations (13) and (14), we calculate the support criterion and the likelihood ratio via below relations:

such that

and

such that

For different values of  and

and , we calculate the value of

, we calculate the value of  according to Equation (12). The results can be observed in Table 1. By carefully considering this table, it is observed that as the value of

according to Equation (12). The results can be observed in Table 1. By carefully considering this table, it is observed that as the value of  increases (which implies the distance growth between

increases (which implies the distance growth between  and

and ), the value of

), the value of  gets closer to one. In other words,

gets closer to one. In other words,  approaches

approaches  more and more. This fact can be interpreted in this way that if the distance between

more and more. This fact can be interpreted in this way that if the distance between  and

and  is large, the data lost in censored data

is large, the data lost in censored data  is negligible. That is to say, evidential inference draws our attention to the time when

is negligible. That is to say, evidential inference draws our attention to the time when  is close to

is close to . The above analysis can also be observed in Figure 1.

. The above analysis can also be observed in Figure 1.

In what follows, the variations of sample volume ratio increase against  are investigated, and the value of

are investigated, and the value of

in the

in the  equation is determined for different values of

equation is determined for different values of  and

and .

.

If  then

then . The result can be viewed in Figure 2, If

. The result can be viewed in Figure 2, If  then

then . The result can be viewed in Figure 3, If

. The result can be viewed in Figure 3, If

then . The result can be viewed in Figure 4.

. The result can be viewed in Figure 4.

The above results can be interpreted in this way that as the sample volume increases from a certain stage on, the value of  remains constant. In other words, it can be intuitively said that the

remains constant. In other words, it can be intuitively said that the  ratio tends to the constant

ratio tends to the constant  value, which this also leads to an increase in evidential strength.

value, which this also leads to an increase in evidential strength.

5. Proofs

In this section,  denotes any constant that does not depend on

denotes any constant that does not depend on  and

and . Its value may change from one term to another and may depends on

. Its value may change from one term to another and may depends on  or

or .

.

Table 1. Computed values for γ.

Figure 1. γ computed from gamma distribution for different values of n.

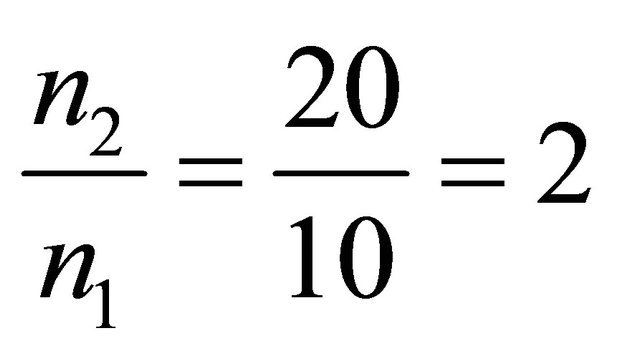

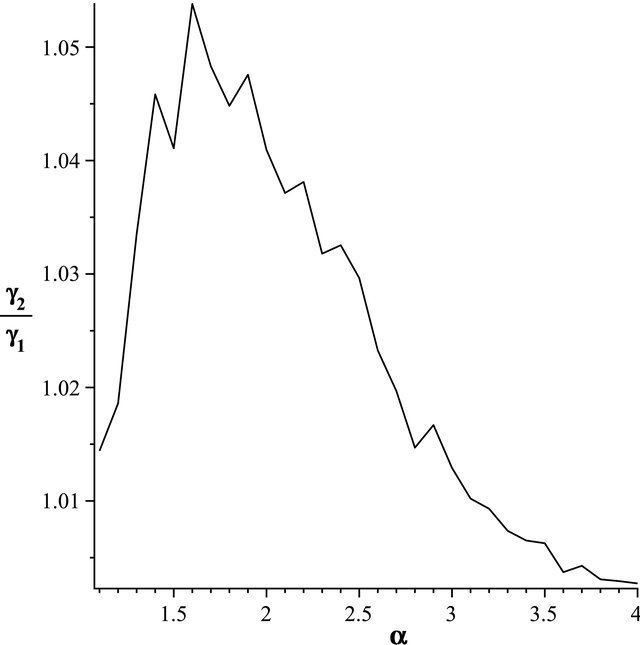

Figure 2. The most relative changes when sample size n1 = 20 increases to n2 = 25 happens in α = 1.6.

Figure 3. The most relative changes when sample size n1 = 10 increases to n2 = 15 happens in α = 2.1.

Proof of Lemma 3.1.

Proof can be found in [13].

Proof of proposition 3.1.

1. By Equation (9) and Equation (5), we have

(15)

(15)

Figure 4. The most relative changes when sample size n1 = 10 increases to n2 = 20 happens in α = 2.2.

Therefore

(16)

(16)

2. By Equation (9) and Equation (5), we have

(17)

(17)

By Equation (4) and under the assumptions of Subsection 2.1 and also doing the change of variables , we have

, we have

(18)

(18)

Using again Equation (4) and the assumptions of Subsection 2.1, the equality

and doing the change of variables , we obtain

, we obtain

(19)

(19)

Combining Equations (17)-(19), we obtain

(20)

(20)

The proof of Proposition 3.1 is complete.

Proof of Proposition 3.2.

1. We have

(21)

(21)

Using Equation (20) we obtain

(22)

(22)

also

(23)

(23)

By the Davydov inequality (see [16]) and for any  we obtain

we obtain

(24)

(24)

Putting Equation (24), Equation (16) and Equation (20) together, we have

(25)

(25)

Since , we obtain

, we obtain

(26)

(26)

Putting Equations (21) and (22) and Equation (26) together, we have

(27)

(27)

2. We have

(28)

(28)

By Equation (5), we have

(29)

(29)

By the Davydov inequality (see [16]) we obtain

(30)

(30)

Combining Equations (28)-(30), we obtain

(31)

(31)

3. Using Lemma (3.1), Equation (27) and Equation (31), then

(32)

(32)

The proof of Proposition 3.2 is complete.

Proof of Theorem 3.1. For any integer , any

, any  can be expanded on

can be expanded on  as

as

where

We obtain

where

Using Proposition 3.2 and inequalitity Equation (11)

and since , we have

, we have . Hence

. Hence

Hence we have

This ends the proof of Theorem 3.1.