H. Miyauchi, T. Misawa

and for the retail sector starts in 2000. Since April 2005, JEPX (Japan Electric Power Exchange) [4] opens a

day-ahead market when the deregulation in retail sector is expanded to the customers over 50 kW.

JEPX operates a day-ahead market for 9 years since then. We have analyzed the prices of JEPX by autore-

gressive model [5]. Though the variables used analyzing other markets are the market price, “System Price” is

analyzed for JEPX because the real market price of JEPX is not open. The system price is a virtual price as-

sumed that the market is unified excluding the different of frequency and congestion in transmission lines.

Moreover, as the every 30 minutes demand is not open in Japan, buying bid data of JEPX is used instead of de-

mand data. That is, the dependent variable of the regression equation is the system price and explanatory va-

riables are the buying bid and the system price of 24 hours ago.

In the analyzing period, JEPX system price is affected by many social phenomena such as Lehman Shock in

2008 and East Japan earthquake disasters in 2011. In this paper, we do not intend to analyze the effect of such

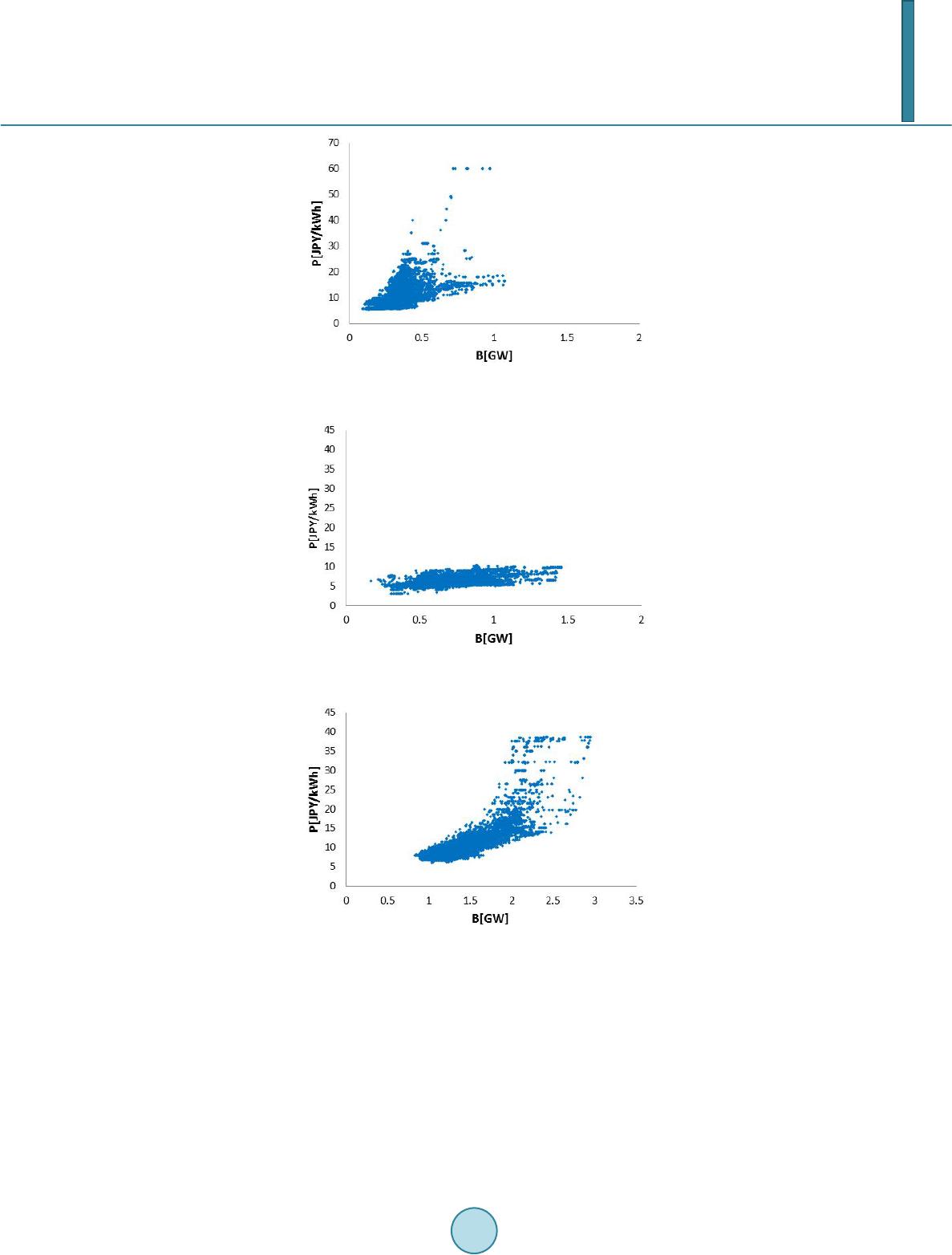

phenomena on the system price. However, autoregressive models of every year are compared and the change of

the price structure is investigated over the years.

2. Analyzed Data

2.1. JEPX Data

JEPX operates the day-ahead market since Apr 2005. Japanese power system is divided to the East Japan system

and the West-Central Japan system due to the difference of frequencies. Only 1200 MW can be transferred be-

tween two different frequency systems by 3 frequency converter sites. Moreover, transmission capacities of the

inter-ties between areas in each syst e m are also small. Then, a market sprit may often occur. JEPX does not

open a real price trading in the market. It opens only “System Price”, which is a virtual price assumed that the

market is unified in the whole country, excluding the difference of frequencies and congestions in transmission

lines. JEPX opens the system price of only two months ago and deletes the data from its open web site at the be-

ginning of the next month. The system price data is every 30 minute data according to the trading conditions of

electricity in Japan.

Demand data is employed in our former analysis for California and so on. However, every 30 minute demand

data is not released in Japan. Therefore, we use the buying bid data of JEPX instead of demand data. We have

already shown the effectiveness of the results using the buying bid data as an explanatory variable instead of

demand data [5].

Though we could obtain the system price data of JEPX from the beginning of its operation in 2005, we can

obtain the bid data of JEPX only from 2007. Therefore, we analyze the price data from 2007 to 2013. In this pa-

per, we analyze data only in summer season, that is, four months from June to September, as the summer is the

peak period of demand in Japan.

2.2. Scattering Diagram

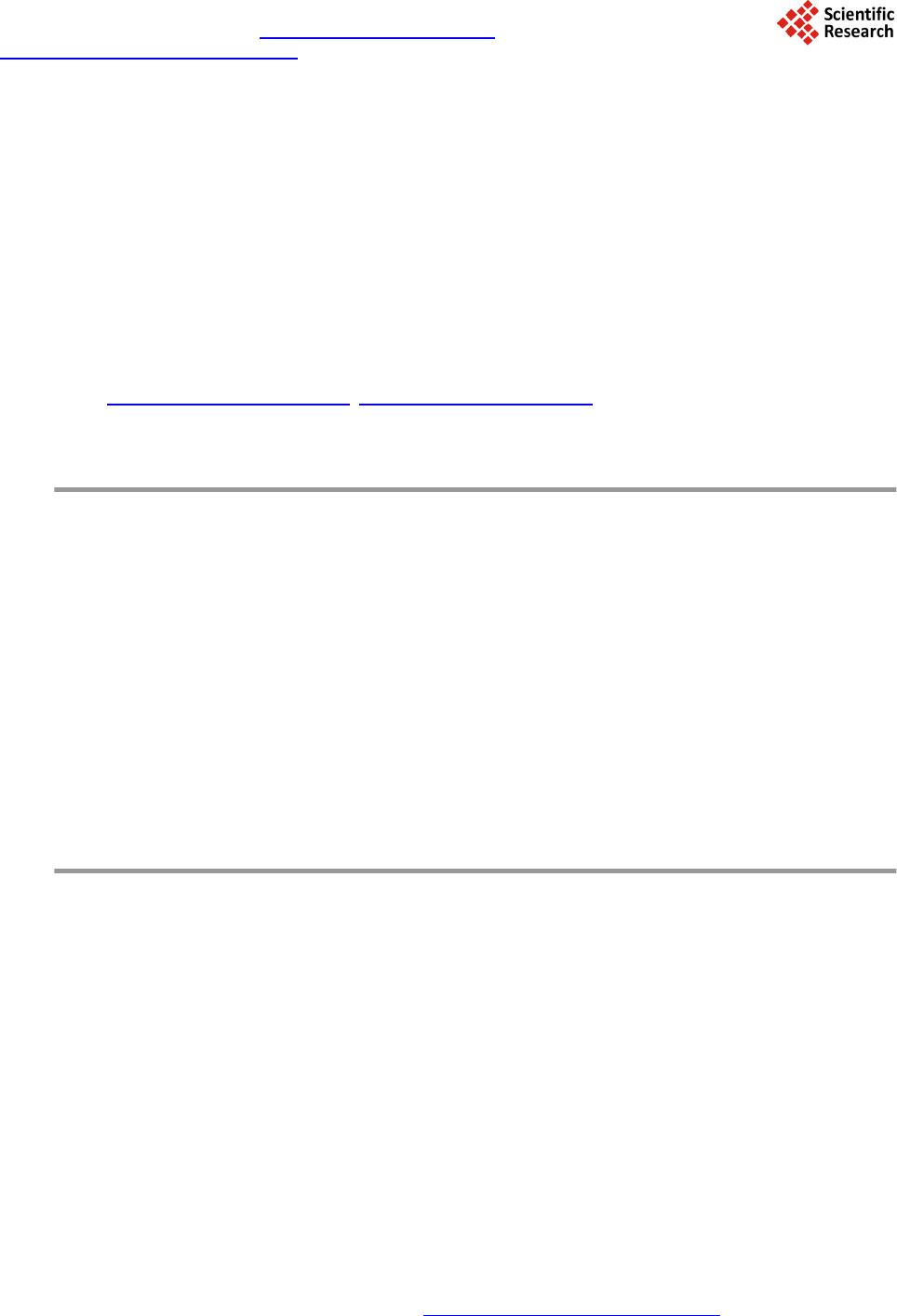

Scattering diagrams between the system price and the buying bid of several years are shown in this chapter.

Figure 1 shows the scattering diagram of the summer in 2007. Though the scale of buying bid is very small,

the system price goes up to 60 JPY/kWh. Fig ures 2 and 3 show the scattering diagrams of the summer in 2009

and 2011. As the Lehman Shock occurred on 15 September 2008, year 2009 is the first year after the Lehman

Shock. The prices are affected severely by the decline of economy. On 11 March 2011, East Japan was attacked

by big earthquake and huge “tsunami” succeeding the earthquake. As many power plants in East Japan including

nuclear power plants were damaged, the electricity was not enough in summer 2011. The system price rises up

to about 40 JPY/kWh when the buying bid rises over 2 GW.

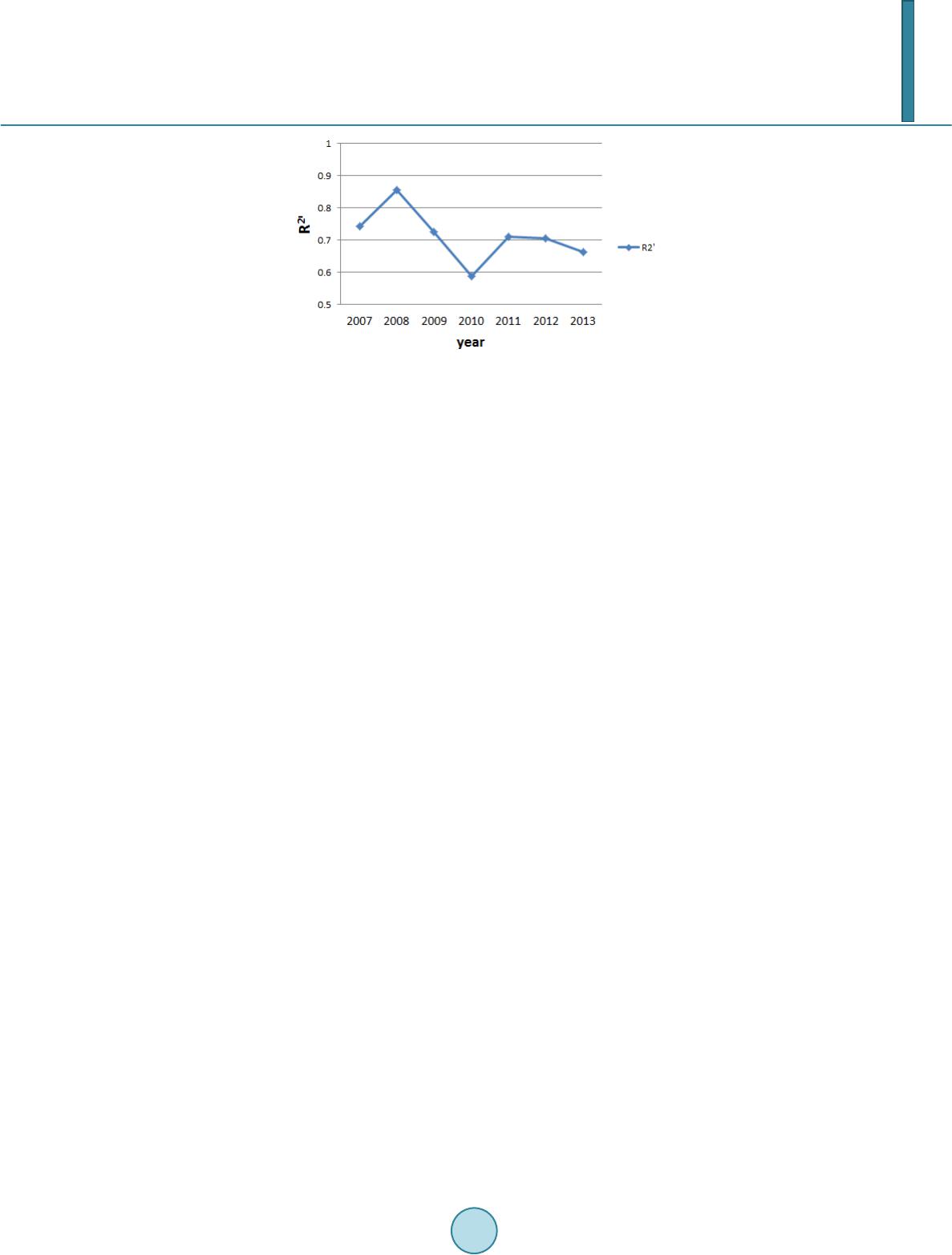

3. Regression Analysis

In this section, the regression equations [6] are derived according to the scattered diagrams shown in the pre-

vious section.

3.1. Regression Equations

We compose a simple regression equation. The dependent variable of the regression equations is the system

price P [JPY/kWh]. The explanatory variables are three variables, that is, the buying bid B [GW], the system