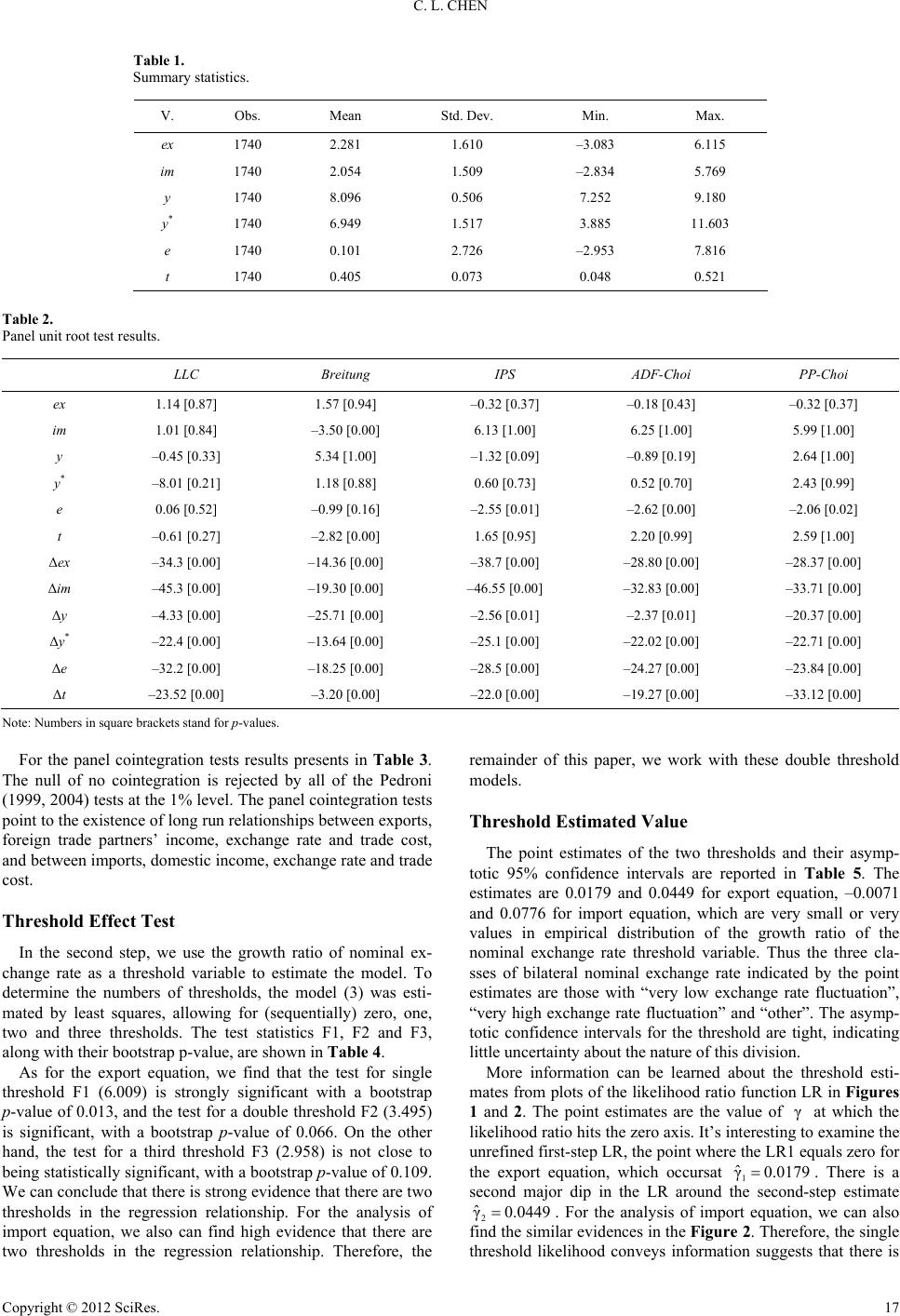

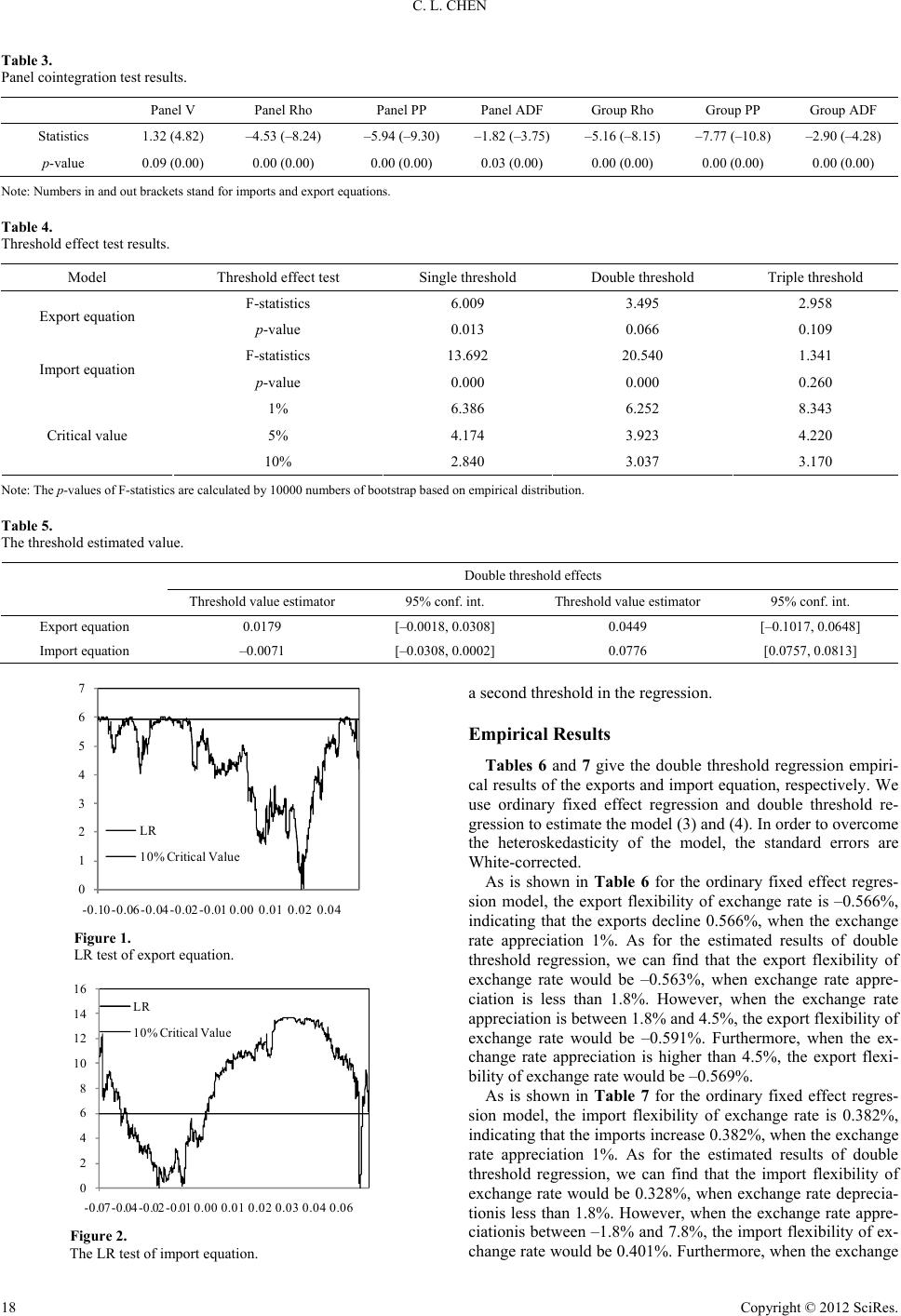

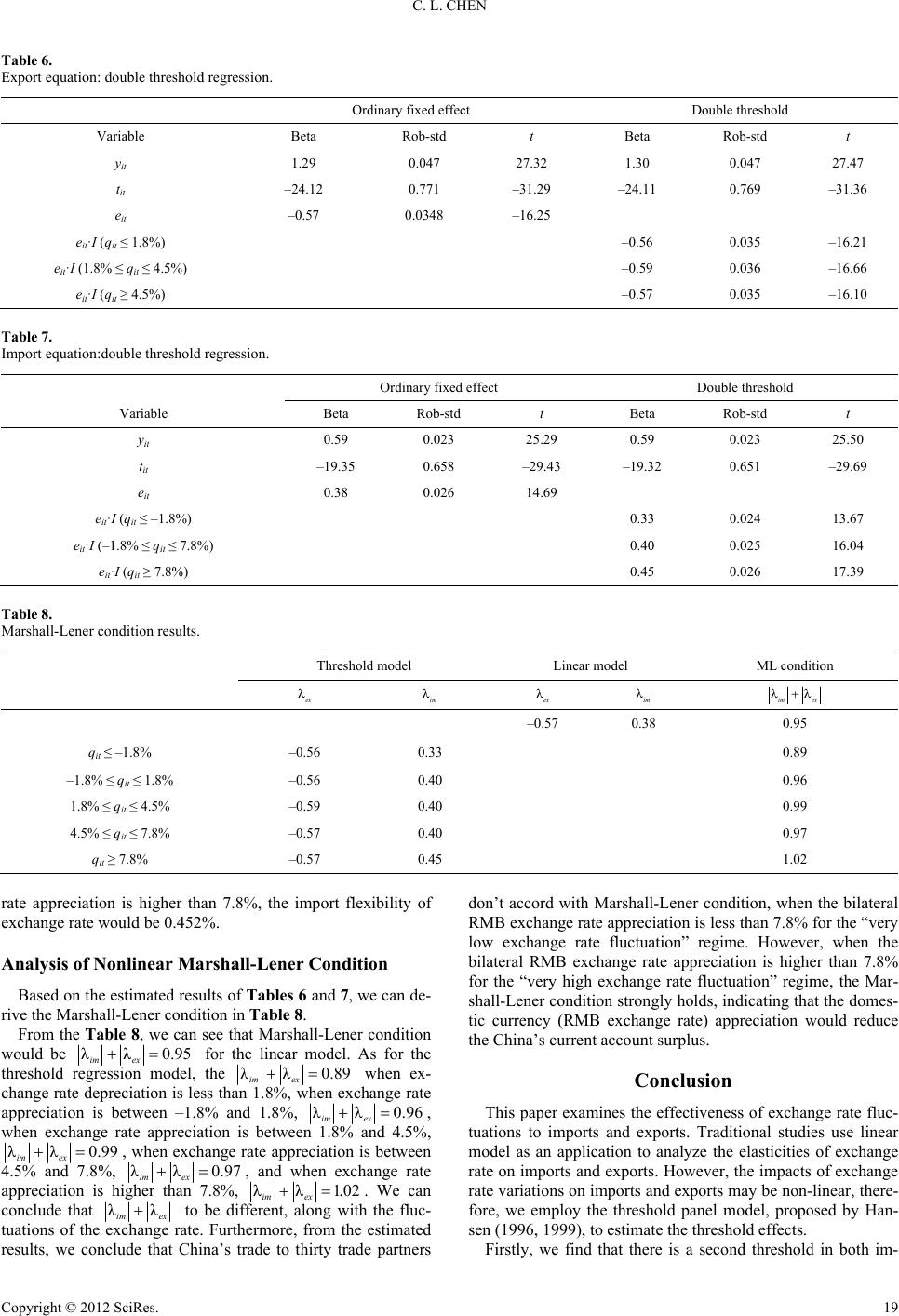

C. L. CHEN

λ0

0δ0

β0

0

β0

im , and exchange rate appreciation would reduce exports

if ex . denotes that trade cost would reduce both

imports and export. im indicates that the improvement of

the domestic income would increase imports, however, if the

domestic income is increased by imports substitution, then

im . indicates that the improvement of the for-

eign trade partners’ income would increase exports, however, if

income is increased by exports substitution, then ex

λ

β0βex

(Kara, 2002). Furthermore, the Marshall-Lener condition holds

if λλ

im ex

1

.

Threshold Panel Regression Model

In order to capture whether there is a structural change rela-

tionship between dependent variable and independent variables.

We use threshold panel regression model, proposed by Hansen

(1996, 1999), as an application. Consider a threshold panel

regression model based on Equations (1) and (2),

2

αβδ 1

λ

λγ

texext it

ex tit

exy t

eIq

ε

ext it

t

eIq

(

3)

2

αβδ 1

λ

λγ

timim tit

im tit

imy t

eIq

ε

im tit

t

eI q

q

(4)

where, it is the threshold variable, representing the growth

ratio of exchange rate.

I

1Iq γq

denotes a Heaviside function,

indicating that it whenit , otherwise,

γ

γIq

1

λim

γS

0

2

λim

it . Equation (3) and (4) are estimated according to

Hansen (1999). When is known, we use ordinary fixed

effect regression model to estimate the values of ex and ex

or and , and the corresponding sum of squared errors

is 1. However, if is un-known, Chan (1993) and Han-

sen (1997) recommend estimation of by least-squares when

non-linear specification of Equation (3) and (4). This is easiest

to achieve by minimization of the concentrated sum of squared

errors. Hence the least-squares estimators of is

γ

γ

1

λ2

λ

γ

γ1

arg min γ

S

1γS

γ

ˆ

γ (

5)

The minimizing sum of squared errors from Equation (5) is

with variance estimate

2

1

ˆˆ

σγ 1SnT

12

:λλH

2

(6)

Then, we have to test whether there is a threshold effect.

Hansen (1996, 1999) provides a hypothesis test, 0exex,

1exex or 0imim, 1imim. Thus an ap-

proximate likelihood ratio test of zero versus single threshold

can be based on the statistic

12

:λλH12

:λλH1

:λλH

2

101

ˆˆ

(λ)σS

S

FS (7)

where 0 denotes the sum of squared errors when null hy-

pothesis holds. The hypothesis of no threshold is rejected in

favor of single threshold if F1 is large. As is pointed by Hansen

(1999), since the null asymptotic distribution of the likelihood

ratio test is non-pivotal, we suggest using a bootstrap procedure

to approximate the sampling (empirical) distribution, and then

derive the bootstrap asymptotic and efficient p-value of the

according F-value under H0. The null of no threshold effect is

rejected if the p-value is smaller than the desired critical value.

Furthermore, Hansen (1996) proves that the statistic p-value

obeys uniform distribution in the large sample, and can be de-

rived through bootstrap.

Finally, we consider the construction of confidence intervals

for the threshold parameters, and then test whether the esti-

mated value of the threshold is a consistent estimator. Due to

the nuisance parameters, the traditional statistics would be non-

standard. In order to overcome this problem, Hansen (1999)

constructs a “no-rejection region” of asymptotic and efficient

confidence interval using the maximum likelihood ratio LR

statistics. Thus we can construct confidence interval to be

2

1111

ˆˆ

γγγσLRS S

1

(8)

Our asymptotic (1–α)% confidence interval for

is the set

γ2log11αLR

such that of values of . One of

the convenient features of this confidence region is that it’s a

natural by-product of model estimation. The likelihood ratio

sequence LR is a simple re-normalization of these numbers, and

require no further computation. The above mode only considers

single threshold condition. In some applications there may be

multiple thresholds. In these cases we can use similar method to

search for the two or more threshold values, pointed out and

discussed by Hansen (1999).

Empirical Results and Analysis

Data Sources

This paper uses data from 1995Q1 to 2009Q3 for China export

to and import from 30 countries and regions1, and quarterly

data are seasonally adjusted by X-12ARIMA. The bilateral real

exchange rate is derived by

RERNRER CPI CPI

CPI

, where

NRER denotes bilateral nominal exchange rate, CPI is the

China’s consumer price index (with 2005 as the base year) and

is the trading partners’ consumer price index (with 2005

as the base year). The trade cost is derived by the following

equation according to Novy (2006),

12ρ2

2

,,,

1

ijij jiijji

TxxGDPxGDPxs

(9)

where, ,ij

denotes the exports of country i to country j.

i denotes the GDP of country i. i

GDP

denotes the exports

of country i. All the data, exports, imports, GDP, bilateral

nominal exchange rate, and consumer price index, are collected

from China’s Economic Internet Database and CEIC Global

Database. The descriptive statistics of the selected variables are

in Table 1.

Panel Unit Root Test and Panel Cointegration Test

The first step is to check for the stationary properties of the

variables involved. Table 2 represents the results of the panel

unit root tests. The level variables have been specified with

individual intercept and trend, and the first difference variables

are specified with individual intercept in the tests. A unit root is

detected for the level variables, while the first differences ap-

pear to be stationary. We conclude that each variable includes a

random walk component.

130 countries and regions include Argentina, Austria, Australia, Brazil,

Belgium, Denmark, German, Russia, French, Philippines, Finland, Kazakh-

stan, Korea, Holland, Canadian, Malaysia, USA, Japan, Swedish, Swiss,

Taiwan, Thailand, Spain, Hong Kong, New Zealand, Iran, Italy, Indonesia,

UK, and Chile.

Copyright © 2012 SciRes.

16