Game Analysis of Institutional Investors Participating in Corporate Governance ()

1. Introduction

Tunneling effect, named by Shleifer, is a common fraud in which controlling shareholders and the management collude to expropriate the interests of minority shareholders. As a countermeasure, China has introduced the institutional investors as an external governance mechanism for better corporate governance. Since the China Securities Regulatory Commission made proposals to develop the mechanism of institutional investors in 2000, a series of policies and measures have been issued to promote its development. Recent years, with the rapid development of institutional investors and their participation in corporate governance, researchers keep wondering, could institutional investors effectively restrain the tunneling behavior? Will they act as active supervisors or bystanders, or will they collude with the management to trample over the interests of the minority shareholders when confronting with the tunneling behaviors?

By building a game model between the institutional investors and the management, we have successfully uncovered the influential factors that are crucial to the role switching of institutional investors when confronting tunneling behaviors of the management.

2. Literature Review

Regarding the role of institutional investors in corporate governance, most of the literatures have proved institutional investors to be active and effective supervisors. Coffee and Barnard are representatives of such hypothesis. They argued that institutional investors are incompetent to play an active role in improving corporate governance structure. In their perspective, institutional investors are not investors but speculators. The pursuit of liquidity has resulted in their preference for short-term investments and diversified investment strategies, which is not acknowledged by the management. At this point, the role of institutional investors is weakened by such internal barriers. Besides, due to the fact that most of the institutional investors have long been engaged in certain capital market operations, the lack of professional knowledge in other related fields keeps many scholars questioning the benefits that institutional investors bring to the listed companies.

So far, most of the domestic studies on split-share reform support the view that institutional investors collude with the management and trample over the interests of the company as a whole. Reference [1] pointed out that from the occurring of Shady Deal of Fund in China in 2000 to profit transfer scandals between public funds and social security funds exposed in 2005, to corruption scandals during split-share reform, people keep raising questions about the role of institutional investors in protecting the interests of minority shareholders and improving market efficiency. Reference [2] studied the determining factors of the split share reform and concluded that institutional investors failed to have bargaining power and thus leaving the interests of the minority investors unprotected. Reference [3] found that the share-holding ratio of the institutional investors was significantly inversely correlated to the stock reform on prices. They explained that non-tradable shareholders colluded with institutional investors to expropriate the interests of the minority investors. Reference [4] conducted a special research on the collusion issues between institutional investors and non-tradable shareholders. They concluded that during the voting process of the share reform program, the support rate of the institutional investors was significantly inversely correlated to the stock reform on prices, which was exactly the evidence of the collusion between institutional investors and non-tradable shareholders. Reference [5] found that the shareholding ratio of the institutional investors was significantly inversely correlated to the consideration ratio of both non-tradable shareholders and tradable shareholders. Based on the findings, they concluded that strategy alignment hypothesis is applicable for the relationship between institutional investors and listed companies. Reference [6] conducted their empirical research in the perspective of managerial displacement. They used data of A-share companies listed in Shanghai and Shenzhen stock exchanges from 2004 to 2008. The result indicated that the shareholding ratio of the institutional investors was inversely correlated to the probability of senior executives being dismissed due to unsatisfying performance. The significant improvement in the company performance after the managerial replacement through internal appointment clearly indicates that institutional investors are responsible for the collusion behind the managerial replacement. Regarding how institutional investors collude with the management, Reference [7] believed that there are three alternatives: 1) the sponsor institution is bribed to vote for the split share structure reform; 2) profit transfer through related business; 3) institutional investors are informed of the insider information beforehand and thus get benefited by means of buying stocks at a lower price.

3. Game Analysis of Supervision and Collusion

3.1. One-Shot Game

In China, the governance structure of the listed companies is not sound, resulting in facts that the due functions of the meetings of shareholders and the boards of directors and supervisors are incomplete. If institutional investors participate in corporate governance, their investment cost may outweigh their gains, which is against their original intention of achieving more gains in corporate governance than in the securities market. Their abundant capital has a conclusive effective on their positions in the shareholders’ meetings. In order to maximize the gains, major shareholders may give up some of their interests and collude with institutional investors to control the operation of the company.

Assumptions of the model are made as follows:

1) Two participants are included in the game model with one as the institutional investor and the other one as the management. The institutional investor is on behalf of the minority shareholders, and the management includes senior managers and controlling shareholders. Both of the participants are rational men pursuing the maximization of their own interests; they make decisions at the same time, aware of each other’s strategies and benefits.

2) The shareholding ratio of the institutional investor is β while the shareholding ratio of the management is θ.

3) The invisible income obtained from tunneling behavior of the management is T, the fine is F if such behavior is caught by the institutional investor, the probability of being caught is α, F > T, 0 < α < 1.

4) If institutional investor colludes with the management, the invisible income T will be shared based on their shareholding ratios. If their collusion is caught, the fine is S, and the probability of being caught is ρ, S > T, S > F, 0 < ρ < 1.

5) The supervision cost of the institutional investor is C and the normal income of the company is R.

Based on the above assumptions, the payoff function and matrix of both sides are shown in Table 1.

Q1 reflects the gain of the institutional investor by conducting supervision on the collusion of the management. If collusion is caught, we could conclude that the interest of the company has been expropriated by the management, resulting in a supervision cost C. If fines are imposed on the management, then the gain of the institutional investor could be calculated as Q1 = β(R + αF – T) – C. Q2 is the gain of the management. Although the management has obtained invisible income, fines have been imposed. Thus, Q2 = θR + T – αF. Q3 reflects the gain in the case of the institutional investor colluding with the management. Although both of profits and invisible income T could be shared, they need to bear certain risk. Thus, Q3 = β(R + T – ρS), Q4 = θ(R + T – ρS). Similarly Q5 = βR – C, Q6 = θR, Q7 = βR, Q8 = θR.

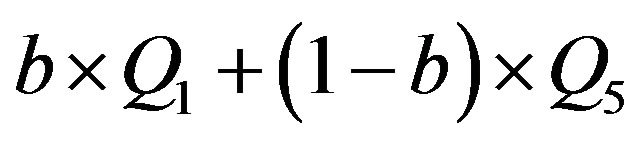

For the institutional investor, suppose the probability of supervision is a, and the probability of collusion is 1 – a. For the management, suppose the probability of collusion is b, the probability of no collusion is 1 – b.

The gain of the institutional investor by conducting supervision is ; the gain of collusion

; the gain of collusion

Table 1. The payoff function and matrix of both sides.

is .

.

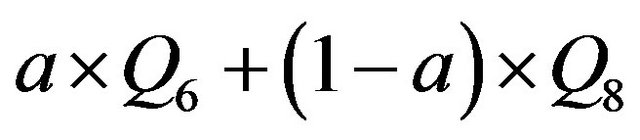

The gain of the management by conducting collusion is ; the gain of no collusion is

; the gain of no collusion is .

.

In such case,  is the equilibrium point of this game, satisfying Equations (1) and (2):

is the equilibrium point of this game, satisfying Equations (1) and (2):

(1)

(1)

(2)

(2)

Then

It can be seen from the above equations that the value of b* is influenced by institutional investors’ supervision cost, shareholding ratio, invisible income and fines. In cases of higher supervision cost, lower shareholding ratios, more invisible income and smaller amount of fines, the probability of collusion is greater. In other words, the loss will outweigh the gain if institutional investors conduct supervision under such circumstance. As a result institutional investors will tend to collude with the management for the maximization of their own interest. Thus, to effectively restrain the tunneling behavior of the management, measures could be taken to lower institutional investors’ supervision cost, increase their shareholding ratios and reduce invisible income through intensive judicial supervision. a* is mainly influenced by the amount of fines and invisible income. In cases of larger amount of fines and less invisible income, institutional investors will tend to play an active role in corporate governance. They will act as an active supervisor to restrain the tunneling behavior of the management.

3.2. Repeated Game

In the one-shot game, every participant only cares about the one-time gain. If the game is repeated, participants may give up the immediate gain for their long term interest and use different balancing strategies. As a result, the frequency of the game would influence the output of the repeated game.

In the repeated game, the institutional investor first determines whether to conduct supervision, and the management makes decision on whether to collude accordingly. In each period, the institutional investor makes decision on whether to conduct supervision based on the gains from the strategy made, which will be added up to the overall strategic gains.

If the institutional investor determines to conduct supervision at the beginning of the game, due to the asymmetric information, the management will determine to conduct collusion with probability of b. But after the first stage of the game, the management will refuse to collude. In such case, the institutional investor’s gain for each period could be calculated by Equations (3) and (4):

(3)

(3)

(4)

(4)

in which σ is the discount rate. The total gain is E = E(1) + E(n).

If the institutional investor determines to conduct no supervision at the beginning of the game, due to the asymmetric information, the management will still determine to conduct collusion with probability of b. But after the first stage of the game, the management will continue the strategy of collusion. In such case, institutional investor’s gain for each period could be calculated by Equations (5) and (6):

(5)

(5)

(6)

(6)

in which σ is the discount rate. The total gain is .

.

Let E = E1, then

It could be seen from the above results that, as compared with the one-shot game the result of the repeated game is influenced by extra factors of time t and σ. Li Xiangqian (2002) believed that σ is an indicator of investors’ patience. A large σ represents more patience of the investors while a small σ represents less patience. In other words, a large σ means that the institutional investors are value investors, and they will tend to restrain tunneling behaviors for long-term gains; reversely, a small σ means that the institutional investors will tend to collude with the management for short-term gains. This viewpoint is consistent with that of Gaspar: institutional investors with longer holding periods are motivated to supervise the management of the company [8].

4. Conclusions

Through the game analysis between the institutional investors and the management, we have successfully uncovered the influential factors that are crucial to the role switching of institutional investors in corporate governance: supervision cost, shareholding ratio, invisible income, fines and patience. In cases of lower supervision cost, higher shareholding ratios, less invisible income, larger amount of fines, more patience and pursuing longterm gains, institutional investors will tend to play an active role in corporate governance. They will act as an active supervisor to restrain the tunneling behavior of the management.

Normally, the board of directors of the listed companies makes the operational decisions. Institutional investors never participate in corporate governance. But most of the equity of the listed companies is in the hands of controlling shareholders while the rest of the equity is scattered. Controlling shareholders could manipulate the operation of the company behind the scenes to expropriate the interests of the minority shareholders. Besides, most of the controlling shareholders of the listed companies speculate in the stock market to hoard capital. Their indiscriminate expansion of the scale has resulted in the unstable development of the securities market. At the end of 2007, China Securities Regulatory Commission approved documents that enable the institutional investors to participate in the board of directors of the listed companies and take part in corporate governance. Since then institutional investors have been playing a role of centralizing the equity of the listed companies to a certain extent. Meanwhile, as a major shareholder, institutional investors could not only restrain the controlling shareholders from benefiting from their control power but also protect the interests of the minority shareholders and maintain the sustainable development of the stock market.

Mark, consultant at the World Bank Group, once said: requirements to develop the mechanism of institutional investors include clearly established legal system, fair investment environment, diversified investment style, professional asset management and smooth sales channels. Thus, in order to motivate the institutional investors to improve corporate governance and protect the interests of the minority shareholders, measures should be taken in the following directions:

1) Relax restrictions on the shareholding ratio of the institutional investors. Currently in China the equity of the listed companies is highly centralized. Relax restrictions on the shareholding ratio of the institutional investors could empower institutional investors more rights to influence the decisions. In this way, checks and balances could be achieved among the shareholders.

2) In order to minimize losses caused by ethical risks, policy making departments should build a complete double principal-agent mechanism between institutional investors and companies. In China most of the funds of the institutional investors are raised from a vast majority of individual investors and thus institutional investors should bear the trust obligation. But institutional investors’ investment behavior is influenced by their own property rights, corporate governance structure and management system. Thus, to prevent institutional investors from seeking profits for self-running investors by violating their trust obligation, property rights of the institutional investors should be clarified to ensure that institutional investors of all kinds unhook connections with self-running investors such as securities companies. Besides, a sound internal governance structure is necessary for the institutional investors. A complete board of directors should be built, independent directors in the true sense should be introduced, and a rigorous internal control system should be built to prevent internal and self-dealing transactions. In addition, most of the institutional investors are evaluated by their short-term performance. As a result, most of the fund managers are motivated to focus on their short-term performance rather than long-term gains, which is against the philosophy of value investment and standards. Too much attention on short-term gains is the cause of institutional investors being speculators rather than investors. In order to further the transformation of institutional investors into value investors and motivate them to play an active role in supervision, the performance appraising system of the institutional investors needs further improvement.

3) Strengthen the development of external environment and create a fair and active investment environment for the institutional investors. Although China has issued a series of related laws and regulations to strength the development of institutional investors, a sound system of laws and regulations in the field of securities is yet to be established. As a result, the legal basis of securities transactions is not solid. Meanwhile, the implementation force of securities laws is inadequate in practice, resulting in violations all the time. Thus, the supervision and management of institutional investors should be strengthened to protect the interests of the minority investors.

5. Acknowledgements

This work is supported by a grant from the Soft Science Project of Guangdong Province: Strategic Research on the Influence of Institutional Investors’ Shareholding to Investment in the R&D of High-tech Enterprises in Guangdong Province (No. 2011B070300059).