Effectiveness of Foreign Exchange Derivatives Usage from Non-Financial Companies: A Brazilian Perspective ()

1. Introduction

The Coronavirus pandemic, alongside with lockdown policies, has generated serious impacts on world’s economy. According to Gomes et al. (2021) , it is estimated a cost of USD 1 trillion at the year of 2020, which is even bigger than the Global Financial Crisis that has affected the world among 2007 and 2008. Scientific studies have shown that the pandemic slowed down world’s economy, reflecting on GDP reductions, which leads to unemployment rates growth and higher public debts.

The lockdown policies, largely adopted worldwide, have resulted in a disruption at the flow of goods, capital, and humans, which has resulted in a negative supply and demand shock at the economy. The early outbreak in China has largely contributed for this unprecedent impact in the global supply chain structure, which is significantly dependent on Chinese manufacturing outputs and raw materials (Barua, 2020) .

The wide range of adversities caused by the pandemic has reflected differently around the world. The study made by Alon et al. (2022) indicates that emerging markets, which have a large part of their workforce concentrated in activities that have a high level of social contact, such as manufacturing and retail trade, have felt an average decrease of 6.7% on their GDP per capita from 2019 to 2020, comparing to 2.4% and 3.6% on developed economies and low-income countries respectively. Not only the macroeconomic impact has been worse for emerging markets, but also number of deaths attributed to the pandemic, being 65 to 75 per cent larger than for advanced economies, according to reliable sources such as The Economist and World Mortality Database of Karlinsky and Kobak (2021) .

Emerging markets are an important part of global supply chains, and they have debts both in local and foreign currency. When compared to advanced economies, they have lower policy credibility, they mostly show heavy dependence on capital inflows to sustain the demands of their growing economies and they operate with low fiscal space. Despite that, their governments increased domestic borrowings, via unconventional policies, to obtain the fiscal resources needed to fight the pandemic, therefore, pressuring their external finance premium, reducing capital inflows and making it harder to roll over their external debt. Those effects could lead an economy into a deep recession, which could be mitigated by a targeted and transparent asset purchase program by its central bank, preserving policy credibility that such programs will not turn into long term monetary financing of government debt (Cakmakli et al., 2020) .

BRICS is a set of emerging markets constituted by Brazil, Russia, India, China, and South Africa, which have faced rapid economic development, and international influence have risen considerably in recent times. As a consequence of their socioeconomics and demographic factors, health and resource vulnerabilities, population mobility and policy response, those countries, as of April 30th of 2021, represented 26.3% of infections by coronavirus worldwide (Zhu et al., 2021) .

According to the Brazilian Institute of Geography and Statistics (IBGE), in April 2020, the industrial production fell 18.8% compared to the previous month, when the first COVID-19 death was officially registered. This early impact of the pandemic raised a warning sign about its consequences, impacting majorly the working class and most companies that were supposed to reduce their overheads as a compensation for the revenue loss (Neto et al., 2022) .

Before going further on the effects of the COVID-19 in the Brazilian economy, it’s important to understand its condition right before the crisis. Oreiro & Paula (2019) indicates that after the period of 2004 to 2013, when Brazilin economy grew at an average rate of 3.80% per year, the country has faced a deep recession within the years of 2014 and 2016, where its GDP has contracted. This strong economic slowdown came along with an acute growth at the unemployment rate, which has jumped from 6.5% in December 2014 to 13.7% in March 2017, keeping at level of 12% in the following months. Those factors are a sign of a stagnated economy that faces a high level of unemployment rate.

In addition to the difficulties that the Brazilian economy was facing prior to the COVID-19, the pandemic brought out the loss of over 2 million job positions, high inflation rate, GDP reduction and other structural issues. These increasing economic effects has risen remarkably tighten credit access, not only in Brazil, but also at global financial markets. At the same time, the government has risen its debt level, in order to stand up to the crisis and stimulate the economy, BRL 500 billion were injected in the economy, as an emergency fund for low-income families. Beyond that, tax collection was postponed, and tax rates were reduced as stimulus for companies (Garbe, 2022) .

Since the moment that World Health Organization (WHO) declared the COVID-19 pandemic on March 11th, 2020, it has occurred an intense growth of the foreign exchange rate USD/BRL. The Brazilian Central Bank has interfered foreign exchange market by selling Dollars in the spot market as a mean of maintaining its liquidity and reduce Real’s intense devaluation. An important consideration is that in moments of crisis the greater liquidity of assets related to hard currencies corroborate with the devaluation of weak currencies, as the market agents naturally look for ways of preserving their liquidity (Bledow, 2021) .

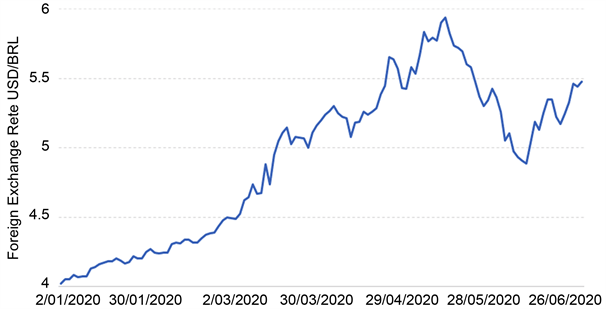

The data provided by Brazilian Central Bank (2023) in Chart 1 illustrate the impact of the pandemic on the foreign exchange rate USD/BRL in the first semester of 2020, where it has increased 47.6% from 4.02 to 5.94 at its peak on May 14th.

Bledow (2021) also indicates that another aspect that needs to be taken in consideration when analysing the Brazilian economy in 2020 is the fact that it was facing a moment of GDP retreat. So, as a manner of stimulating the economy, the Central Bank kept the interest rate at lower levels, reaching 2% per year from August 2020 to March 2021, the lowest interest rate experienced since the Real has been adopted as official currency.

Furthermore, the Brazilian fiscal rules have been through an unprecedent

Chart 1. Foreign exchange rate USD/BRL evolutive (02/01/2020-30/06/2020). Source: Banco Central do Brasil (2023) . Elaborated by the author.

flexibilization, a strong pack of fiscal stimulus were fast paced implemented to face the needs of the sanitary, economical and social crisis faced. In 2020, a “war budget” was approved, free of the usual fiscal restrictions, as a manner of immediately respond to the pandemic. Government’s primary expenses have totalized BRL 520.6 billion, which correspond to 7.0% of the GDP in the year of 2020; this amount was allocated for public health care resources, assistance for low-income families, credit subsidy for enterprises and support for states and municipalities. Besides that, initiatives that reduced government’s revenue were also implemented, such as tax relied (around 0.4% of GDP) and postponement of some of their receivables (Orair, 2021) .

Given the macroeconomic scenario that was set, the main challenge for enterprises that operates in Brazil was to reflect the crisis impact on their business continuity and on their financial statements, affecting the reconciling, the recognition and the publication of their assets, liabilities, debts and revenue. In a broader perspective, taking in consideration the companies that are listed in the Brazilian stock market (B3), the comprehensive income and net profit have reduced, when comparing the years of 2019 and 2020, whilst they have increased when comparing the years of 2021 and 2020 (Colares et al., 2022) .

The article is organized as follows: besides this introduction, the Section 2 we present the literature review that goes over the use of foreign currency derivatives for risk management. Afterwards, the methodology section describes the data collection, the descriptive analysis and the econometric study, followed by their results and robustness analysis. At last, it is exposed the final considerations regarding the study.

2. Literature Review

Macroeconomic and currency crisis almost always affect the economy’s relative prices, for example impacting firms’ investment propensity. In some studies firms that hold more dollar debt invest less in the wake of currency devaluation, as per the balance sheet losses they face. Taking in consideration previously experiences, as the Brazilian currency crisis of 2002, when the Brazilian exchange rate fell approximately 53% in relation to the dollar, firms that had heavy unhedged foreign debt suffered enormous financial losses and the cost of financial loans rose considerably, the rollover rate for foreign currency debt fell, indicating tighter credit conditions (Janot, Garcia, & Novaes, 2008) .

Business managers have made significantly efforts trying to comprehend how COVID-19 would impact their business and the best manner to deal with it. The way the pandemic impacted Brazilian enterprises could be observed at the information presented on their respective financial statements. The pandemic has drastically reduced the economic activity, resulting on a decrease of the companies’ revenue level, and was observed a systematic decrease in the profitability indicators, independently of the calculation method. As the revenue reduced, it was expected a greater necessity of resources to finance their operations, which was observed in the increasing of debt level, considering multiple methods of analysing their capital structure. On the other hand, their liquidity does not present significant variations (Ewerton et al., 2021) .

There are theoretical backgrounds which indicate that risk management increases firm value at uncertain times of financial distress. Risk management initiatives are more likely to be implemented in firms with higher foreign debt proportions, more investments through Capex and higher growth opportunities. Firms that present an important proportion of foreign currency debt to finance their operations have the possibility of using currency derivatives for hedging as a risk management tool (Gatopoulos & Loubergé, 2013) .

Currency derivatives usage for hedging purposes is a well-known mechanism to mitigate foreign exchange risks and it can increase a firm’s valuation by increasing its debt capacity, increasing its market value and shareholder value consequently. It is likely to be applied when enterprises face certain circumstances, such as financial distress costs, growth options, investment opportunities and future cash flow needs. In general, derivative users tend to have high foreign exchange exposure, higher debt, and short-term liquidity, and also are significantly larger in size than the non-users (Lee, 2019) .

At first, the use of foreign currency derivatives might seem like an obvious choice, as it helps to make the future cash flows of an enterprise more predictable, helping to guarantee liquidity and solvency, which are key factors for business continuation. Also, mitigating risks, such as foreign currency volatility, allows the enterprise to focus its efforts at their core business, where they are expected to have the technical knowledge for decision making. However, the market risks are not totally extinct as a hedge instrument is contracted. The accounting rules requires that derivatives contracts need to follow the mark to market method, when recognized at companies’ financial statements, which means in case of events that requires liquidity before the derivative maturity, the foreign exchange rate contracted will be adjusted according to market current conditions, allowing unexpected risk exposure. This complexity hold off smaller companies that don’t have the technical knowledge to operate such instruments (da Silva, 2022) .

Previous works have been done in order to evaluate derivatives usage by non-financial companies:

The work published by Bartram, Brown and Fehle (2009) claims to be the first comprehensive global examination of hedging practices and has analysed a database of 7.319 firms within 50 countries, this sample was made by matching firms’ accounting data on the Thonson Analytics database and the Global Reports database for the years of 2000 and 2001. Alongside with an automated search using a concordance for 37.537 expressions presented on firms’ annual reports, they were classified as derivative users or not. Across the entire sample, 60.3% of the firms use some kind of derivative, being the most common the foreign exchange rate derivatives (45.2%), followed by interest rate derivatives (33.1%) and in third commodity price derivatives (10.0%). The study also reinforces that most of the time hedgers are larger companies, more profitable and have longer debt maturity.

The article published by Saito and Schiozer (2007) presents the results of research analysing the usage of derivatives by Brazilian non-financial companies that are listed in the Brazilian stock market. In March 2004, an invitation was made by e-mail for 378 companies, of which 74 has agreed to take part of the research. The study found out that from the 37 companies, which the assets value were above the median of the sample, only 3 claim to not use derivatives, while in the other half of the sample, only 8 companies claim to use derivatives. From the companies which affirm to use, 96.7% use foreign exchange derivatives, 83.3% interest rate derivatives and 35.7% commodity price derivatives. Also, the study found out that most Brazilian companies employ profitability metrics to evaluate the effectiveness of risk management, which can mislead the use of derivatives; however, they are not frequently used for speculative purposes.

The study made by Janot, Garcia and Novaes (2008) tested the transmission mechanism for balance sheet losses using a database that allowed to measure currency mismatches, which is defined as foreign currency debt net of foreign currency assets and derivatives, of publicly held Brazilian firms between 2000 and 2004, this period includes the Brazilian currency crises of 2002. This article aimed to investigate the drop in investment rates by firms with unhedged foreign currency debt resulting from currency depreciation, by dividing the firms in two groups, being the treatment group composed of firms with unhedged foreign debt and the control group composed of firms without currency mismatches. As a result, the study support that there is a sharp drop in aggregate investment during currency crises, when there is a relevant amount of firms with unhedged foreign debt.

The work elaborated by Borgheti, Santos and Lima (2020) investigates if the use of derivatives to mitigate market risks generates value for the enterprises. The sample consists of all non-financial Brazilian companies that are listed at the Brazilian stock market within the years of 2010 and 2014 and the data were manually collected through the annual reports of such companies, dividing the companies in two groups of derivative users and non-users. Five variables were chosen to evaluate the two sets of companies, being them: size, current liquidity, financial leverage, profitability and investment opportunity. The results show that derivative users are bigger in size, more profitable and are more financially leveraged, while non-users have greater current liquidity and investment opportunity.

In summary, there are opportunities that can be explored in the studies cited above. The first study lacks investigating the effectiveness of the hedging instruments utilised by the selected companies. The second works with a relatively small sample and its results depends on the trustworthiness of the answers provided by each company. The third study evaluates firms’ value by the optics of investment, instead of analysing profitability and financial return metrics. The fourth comprehends a period of majorly economic stability, where the macroeconomic scenario does not significantly defy the Brazilian companies’ risk management decisions.

The objective of the present study is to evaluate the financial statements of the Brazilian companies that are listed at the Brazilian stock market (B3) and had foreign currency indebtedness during the period of 2019, 2020 and 2021, given the unprecedented macroeconomic scenario, to understand whether the use of foreign exchange derivatives for hedging purposes have generated value or not, considering companies that have debt in foreign currency.

3. Methods

The research consists of an exploratory study of the financial statements and annual reports of the listed Brazilian non-financial companies, followed by a descriptive statistical analysis. As a manner of validating the proposed hypotheses test, an econometric equation was stablished.

The first part of the present study is to analyse the financial statements and annual reports of the Brazilian non-financial companies which are listed at B3. The financial statements were obtained via Economatica platform, and the annual reports were obtained at the Investors Relators page of each company. Financial companies were not included in this study, as commonly use derivatives for other purposes apart from hedging.

Once all data were collected, an exploratory search was made, in order to identify the following information regarding the companies that take part of this study: their debt in foreign currency, their total assets, their net profit and if they use foreign exchange derivatives for hedging purposes. The search was made for each quarter of the years of 2019, 2020 and 2021 separately, the year of 2022 was not considered in the analysis, because companies’ annual reports have not yet been published by the time data were collected. The following key words were selected to make it feasible to search the financial statements and classify all companies, being them: derivative, risk, exchange, exchange rate.

The results of this search were used to fulfil a table with information for each company in each period of study; this table was set as reference for further analysis. After setting up the reference table, descriptive statistical analyses were made as a method of being able to understand and criticise the resultant data from the exploratory search that was made. Also, for the purpose of running an inferential statistical test with the collected, the following two hypotheses were determined:

Null hypotheses (H0): the use of foreign exchange derivatives for hedging purposes in the context of the COVID-19 pandemic have not generated value for the enterprises.

Alternative hypotheses (H1): the use of foreign exchange derivatives for hedging purposes in the context of the COVID-19 pandemic has generated value for the enterprises.

A Student’s t-test was made as a method of verifying which of the two hypotheses should be accepted.

Econometric Study

To test the hypothesis that the use of foreign exchange derivatives for hedging purposes in the context of the COVID-19 pandemic have generated value for the enterprises, a model was estimated, taking into account foreign currency indebtedness as a control variable. The selected dependent variable for this study is ROA (Return on Assets), defined as a company’s net profit divided by its total assets during a specific period (Ross et al., 2022) . The choice of this dependent variable allows for the comparison of companies’ profitability during the study period.

Based on the previous study of Bleakley and Cowan (2008) , the following control variable was determined:

Foreign Currency Debt Variation:

Being:

· D: debt in foreign currency.

· Δe: USD/BRL variation during period t.

· TA: Total Assets.

At last, the dummy variable (Der) was determined as a manner of indication if a company have used or not derivatives for hedging purposes at a given year.

Given the set of variables that were determined above, the following econometric equation was built:

where i corresponds to the companies analysed and t corresponds to the years comprehended in the present study. The objective of this equation is to determine if the use of derivatives has impact on companies’ value generation and also to assess if control variables have adherence to the proposed model.

Following the methodology proposed by De Moraes, Barroso & Nicolay (2018) , those objectives were checked by solving the Fixed Effects econometric method. Subsequently, the robustness of the model was tested by solving the same equation with the Random Effects method.

According to Wooldridge (2015) , the Fixed Effects estimator allows for arbitrary correlation between the unobserved effect and the control variables in any period of time. Because of this, any control variable that is constant over time for all i gets swept away by the fixed effects transformation:

= 0 for all i and t, if

is constant across t. On the contrary, the Random Effects estimator assumes that the unobserved is uncorrelated with all the explanatory variables, whether the explanatory variables are fixed over time or not.

At last, a Hausman Test was performed to determine which method best fits the proposed model. Also known as the exogeneity assumption, the Hausman test provides statistical evidence that unobserved individual effect is correlated with the conditioning regressors in the model. The rejection of the exogeneity assumption indicates that the Fixed Effects method best fits the model over the Random Effects method (Amini et al., 2012) .

All data treatment and testing were made with the assistance of Python programming language.

4. Results

4.1. Sample Definition

The sample defined for this study consists of non-financial companies that were listed in the Brazilin Stock Market (B3) within the period that comprehends the years of 2019, 2020 and 2021, being the last two years severely impacted by the COVID-19 pandemic. The year of 2019 was also selected to allow the study to compare the descriptive statistical results before and after the pandemic outbreak.

Starting off from the initial sample, a total of 18% of the observations were excluded from the study, as there was no sufficient evidence of whether the company used derivatives for hedging purposes or not. Lastly, there were about 58% of the observations that have shown no amount of debt in foreign currency. It is also important to highlight a limitation factor of this study that several companies do not specifies if their debt is composed of domestic or foreign currency.

From the final sample of 695 observations, it was verified that 65% of them consisted of companies that used derivatives for hedging purposes and 35% of companies that does not used derivatives for hedging purposes.

Table 1 and Table 2 summarize the data gathering results:

4.2. Descriptive Analysis

A descriptive analysis was performed in order to better understand the final sample of 695 observations and to help answering the question proposed at the present study.

Starting off by Table 3, it was observed the percentage of observations that corresponded to derivative users for hedging purposes at each year of analysis. It could be observed that at the year of 2019, before the pandemic, about 61% of the companies that had debt in foreign currency used derivatives to protect their respective cash flows and balance sheets from losses originated from foreign currency fluctuations. Progressing to the years of 2020 and 2021, the percentages have increased to 64% and 70% at last.

Those results provided initial evidence that more companies looked for protection from currency fluctuations during the pandemic, therefore trying to preserve their value generation. However, it is important to note that the Brazilian Central Bank interfered in the economy providing better conditions for companies that were exposed to exchange rate variation, selling US Dollars at the spot market, and offering exchange rate swaps (Bledow, 2021) .

Moving forward with the analysis, the companies were classified according to the sector of the economy they belong to; those sectors were previously defined by the Brazilian Stock Market (B3).

Analysing Table 4, it was found that the companies that take part of the present study belong to 8 different sectors of the economy, where about 80% of the observations are concentrated at cyclic consumption, industrial goods, basic materials, and non-cyclic consumption sectors. The sectors where proportionally more companies using derivatives for hedging purposes were observed were communication, health and non-cyclic consumption, at those sectors, derivatives were applied in more than 80% of the observations. At last, it is important to punctuate that in 7 of the 8 sectors derivatives were used in more than 50% of the observations.

Table 5 provides quantitative information about the sample analysed at this study. The Total Assets (TA) indicates that the sample is composed of a heterogeneous range of companies, as the smallest company had BRL 42.4 million in assets, while the biggest had BRL 207.1 billion in assets. The Net Profit presents

![]()

Table 3. Percentage of derivative users in the sample per year of study.

![]()

Table 4. Number of observations and number of derivative users per economic sector.

![]()

Table 5. Descriptive analysis of the sample.

that, while some companies had made significant profit during the period of study, there were companies facing expressive loss, contributing to heterogeneity of the sample. Analysing the Foreign Currency Debt, the data show that while there were companies presenting a small amount, there were ones with expressive debt.

Table 6 summarises quantitative information regarding the dependant and control variable. Following the pattern found in the total assets and net profit, it was found a wide range of ROA, which reinforce the heterogeneity of the sample. Regarding Foreign Currency Debt Variation, it was found a heterogeneous result with companies that had little of their debt impacted by currency foreign currency fluctuation, while other companies had a significant impact.

![]()

Table 6. Descriptive analysis of the dependent and control variables.

Table 7 presents the results of a t-statistics test ran for the data sample during the 3 years of observation. The objective of this test was to assess if with 95% of confidence, the null hypothesis presented at this study should be accepted of not. According to the t-values found for each year, being then bigger than the critical value for every year, the null hypothesis should be rejected, which means that there was evidence of companies which used derivatives for hedging purposes having a higher ROA than the ones that had not used derivatives.

4.3. Econometric Analysis

After running the descriptive analysis, in order to better understand the data sample, the econometric regression analysis was run. The regression analysis was made using the Fixed Effects method, to understand how each control and dummy variables fit the equation. The Fixed Effects method was applied using Python Programming Language and its results are presented in Table 8 and Table 9 bellow.

Table 8 presents the overall picture of the regression analysis. It specifies the dependent variable as ROA, the method as the Fixed Effects and the number of observations that were provided to the model, in order to reach the obtained results.

On the right-hand side of Table 8, it presents the indicators that measure the significance of the model. Analysing the R-squared, as it is defined as the proportion of the variation in the control variable in the population that is explained by the control variables (Bleakley & Cowan, 2008) , the results suggest that a small proportion of the variation in ROA is explained by the model. Nonetheless, when analysing and the Probability of F-statistic, as the F-statistic determine the overall significance of a regression (Wooldridge, 2015) , the value below 0.05 indicates a good acceptance of the regression model.

Table 9 provides the significance and the coefficients for each control variable, as it is interpreted bellow:

1) Foreign Currency Debt Variation: the p-value under 0.05 indicates that the variable is significant for the model. The negative coefficient indicates that the larger companies’ foreign currency indebtedness is, the more it is expected to fluctuate under conditions of foreign currency volatility and the greater is going to be the negative impact on their profitability in periods of local currency devaluation.

![]()

Table 7. t-statistics test for each year of analysis.

![]()

Table 8. Panel OLS regression results.

Note: **denotes a significance level of 0.05 and ***denotes a significance level of 0.01.

2) Derivative: the p-value under 0.05 indicates that the variable is significant for the model. The positive coefficient suggests that there is indeed a positive correlation within the use of foreign currency derivatives and the generation of value for companies that have foreign currency indebtedness, once the regression analysis suggests that it increase companies’ ROA.

4.4. Robustness Test

In this section, the study explores the robustness of the results found at the regression analysis. In order to perform this test, the model was tested again with the Random Effects estimation method. Table 10 and Table 11 bellow show the new estimation results.

The new estimation with Random Effects reinforces the results found with the Fixed Effects estimation. The positive coefficient for the variable Derivative provides more evidence that companies’ profitability increases when they use derivatives to manage the exchange rate risk at their foreign debt.

![]()

Table 10. Random effects regression results.

Note: **denotes a significance level of 0.05 and ***denotes a significance level of 0.01.

At last, Table 12 provides the results of the Hausman Test that was performed to assess which of the two estimation methods best fit the proposed model. The p value under 0.05 indicates that exogeneity assumption should be rejected, so the Fixed Effects should be the method which best fits the proposed model.

5. Conclusion

The macroeconomic scenario has indeed induced the Brazilian companies, which had foreign currency indebtedness to acquire foreign currency derivatives for hedging purposes. Companies’ behaviour in this unprecedented scenario of pandemic, corroborates with the theoretical background, where firms’ management seeks for value increase in risk management.

While constructing the data base for the present study, the main challenge face where the quality of the data available regarding short and long-term foreign currency indebtedness. According to the data available at the Economatic platform, several companies do specify whether their indebtedness is in local or foreign currency. This fact resulted as a limiter for the study, as the resultant sample space has considerably reduced, when compared to the one that was proposed at the beginning of the exploratory research. Also, the data regarding the use of derivatives were collected directly from the explanatory notes presented in the firm’s financial statements, a process where some erroneous interpretations may occur.

Even though some limitations were faced in the stage of construction of the data base, the available data were sufficient to obtain satisfactory results. The Fixed Effects test presented satisfactory adherence and allowed the study to infer that there is evidence that the use of derivatives during the COVID-19 pandemic have indeed increased firm’s profitability.

In summary, the present study has the aim to contribute with the existing literature regarding risk management and the results found are important to reinforce the theoretical background that risk management has relevant effect on firm’s profitability. At last, the availability of better-quality data regarding risk management and foreign currency exposure provided by companies in future financial statements could have significant impact on helping future studies.