1. Introduction

Banking sectors in Eastern and Central European countries have undergone major transformations over the past two decades, firstly, as a consequence of the transition from centrally planned economy to market economy and, secondly, due to the European integration process. These processes led to the establishment of specific regulations for banks and other financial intermediaries which allowed their modernization and rapid changes in their ownership structures. At first, capital flows were characterized by privatizations and mergers and, subsequently, by the entry of foreign ownership into the industry.

Some studies [1-3] have found evidence of clear improvements in the banking performance of transition economies since the adoption of the new regulations and, especially, since the massive entry of foreign ownership. However, when the studies focus on how changes in bank ownership structure affect the performance of individual banks in these countries, the results are not so clear. While some of them [1,3,4] found that foreignowned banks are more efficient than their domestic counterparts, other studies [5,6] found no evidence of this. It should be noted that most of the studies cited focus on the transition period (1990s) and the years immediately preceding the 2004 enlargement, while only a few studies have worked with more recent data including the years immediately following their accession.

In this article, we analyze the banking efficiency levels estimated for each group of private ownership (we have excluded public ownership because the empirical evidence has reached a certain consensus on its lower levels of efficiency compared to private ownership; [1,7]). We also analyze the impact on banking efficiency levels of incorporating a strategic foreign owner into the ownership structure. In this way, we hope to provide empirical evidence about whether, as popular belief would have it, foreign banks are more efficient than their domestic counterparts or whether, as a consequence of the European integration process, these differences have gradually disappeared.

2. Data

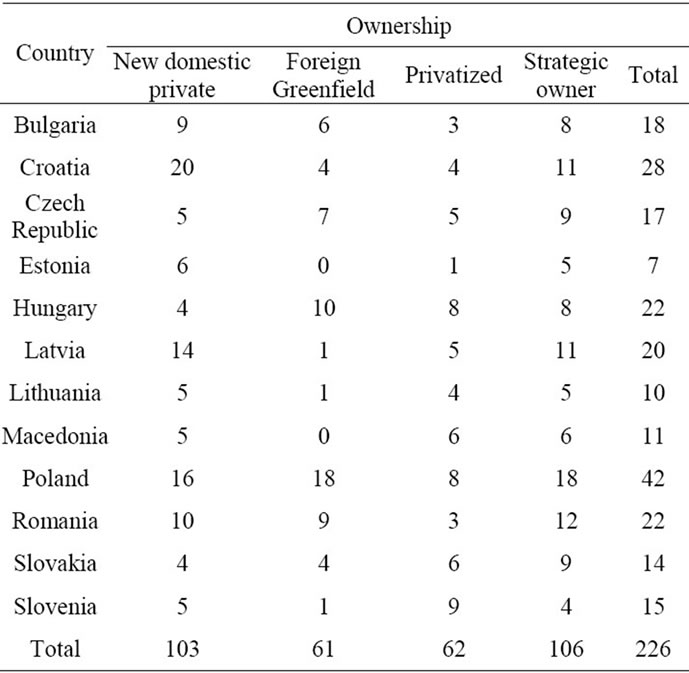

Balance sheet and income data are taken from the Bureau Van Dijk’s BankScope data base. Specifically, we have chosen all currently active private commercial banks in the 12 countries that have experienced the European integration process more intensely in recent years and for which there are data available for all necessary variables for the estimation of efficiency levels for at least one year between 2000 and 2008. This period was chosen because of the intensification of the European integration process experienced by central and eastern European countries during these years. In total, the dataset consists of 226 banks.

In Table 1, we can see the composition of the sample by ownership types and by countries; it also shows the presence of strategic owners in the sample. Banks are divided into three mutually exclusive and collectively exhaustive private ownership types, namely, foreign Greenfield banks, new domestic private banks and privatized banks.

Table 1. Distribution of banks across bank types by country.

3. Methodology

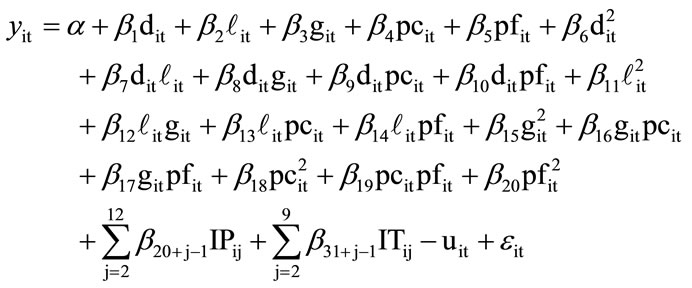

In order to estimate the cost and profit efficiency of a bank, we have used stochastic frontier models. We have opted for the added value approach [8] and following [1] we have used three outputs: deposits (D), loans (L) and other earnings assets (G), and two input prices: capital price (CP), measured by the ratio of total operating expenses over fixed assets, and fund price (FP), measured by the ratio of financial expenses over total deposits.. Our dependent variables are total cost (C) for cost efficiency and profits before taxes (B) for profit efficiency.

We have used a translog specification for the model with fixed effects for each country and year. So, if “i” denotes the bank and “t” the period, the equation of the model is given by:

if yit = log(Cit) and

if yit = log(Bit), where dit = log(Dit);  = log(Lit); git = log(Git); pcit = log(PCit); pfit = log(PFit); IPij and ITij are indicators of the j-th country and the j-th period, respectively; uit is the inefficiency term; eit ~ N(0, s2) is the error and t Î Ti,

= log(Lit); git = log(Git); pcit = log(PCit); pfit = log(PFit); IPij and ITij are indicators of the j-th country and the j-th period, respectively; uit is the inefficiency term; eit ~ N(0, s2) is the error and t Î Ti, ; i = 1,

; i = 1, , N where Ti is the observation period of the i-th bank and N is the number of analyzed banks.

, N where Ti is the observation period of the i-th bank and N is the number of analyzed banks.

We have assumed that  ~

~ , (g’wit,

, (g’wit, ), where wit = (wit1,

), where wit = (wit1, , witk)’ are the explanatory characteristics of bank inefficiency and g = (g1,

, witk)’ are the explanatory characteristics of bank inefficiency and g = (g1, , gk)’ a vector of parameters that quantifies their influence on the efficiency level rit =

, gk)’ a vector of parameters that quantifies their influence on the efficiency level rit = .

.

In order to estimate the parameters of the model we have used the Bayesian approach described in [9] that allows us to make exact inferences about them.

4. Results

Table 2 and Figures 1 and 2 show the estimated mean cost and profit efficiency levels for the three types of ownership mentioned above. They are very similar for both cost and profit efficiency, the most outstanding result being the complete lack of significant differences between them. This result suggests that, nowadays, ownership type is no longer a determinant of banking efficiency in these countries.

Table 3 shows the estimated mean cost and profit efficiency levels for the banks before and after the incorporation of a strategic foreign owner. A very small increase in cost efficiency can be appreciated after the incorporation of a strategic foreign owner. In contrast, profit efficiency is basically unaltered after this incorporation. In both cases we note, however, that the most outstanding result is the complete lack of significant differences between the efficiency levels estimates for banks before